David Glasner is one of an increasing number of Fed critics who would like to see a higher inflation target. Today, he takes aim at a Wall Street Journal editorial that claims that the real victims of cheaper money wouldn't be, you know, people who own money -- creditors -- as one might think, but working people. Higher inflation just means lower real wages, says the Journal. Crocodile tears, says Glasner -- since when does the Journal care about wage workers? So far, so good, says me.

"What makes this argument so disreputable,"he goes on,

is not just the obviously insincere pretense of concern for the welfare of the working class, but the dishonest implication that employment in a recession or depression can be increased without an, at least temporary, reduction in real wages. Rising unemployment during a contraction implies that real wages are, in some sense, too high, so that a falling real wage tends to be a characteristic of any recovery, at least in its early stages. The only question is whether the falling real wage is brought about through prices rising faster than wages or by wages falling faster than prices. If the Wall Street Journal and other opponents of rising prices don’t want prices to erode real wages, they are ipso facto in favor of falling money wages.And here we have taken a serious wrong turn.

Glasner is certainly not alone in thinking that rising prices are associated with falling real wages, and vice versa. And he's also got plenty of company in his belief that since the wage is equal to the marginal product of labor, and marginal products should decline, in the short run higher employment implies a lower real wage. But is he right? Is it true that if employment is to rise, "the only question" is whether wages fall directly or via inflation? Is it true that unemployment necessarily means that wages are too high?

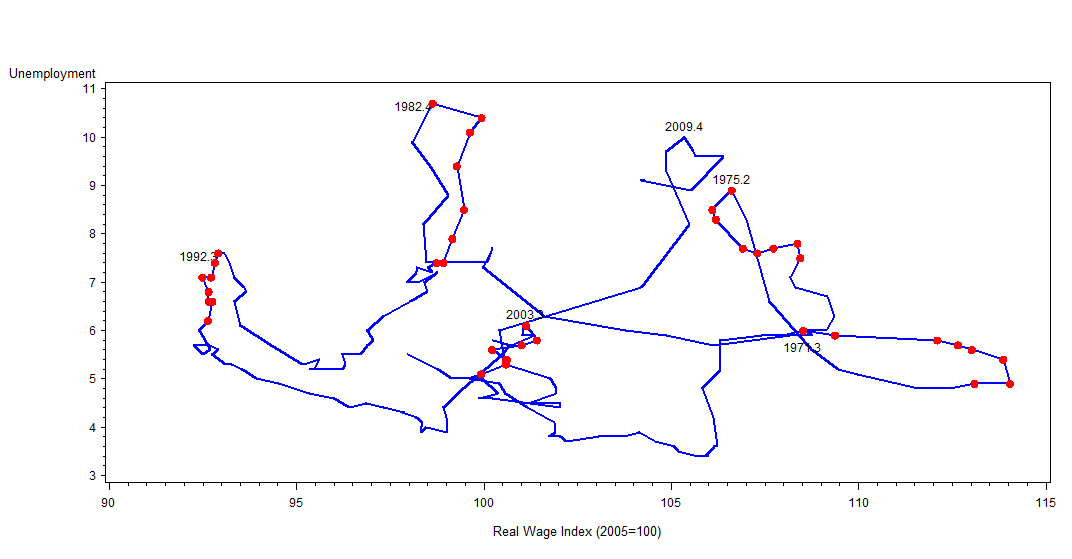

Empirically, it seems questionable. Let's look at unemployment and wages in the past few decades in the United States. The graph below shows the real hourly wage on the x-axis and the unemployment rate on the y-axis. The red dots show the two years after the peak of unemployment in each of the past five recessions. If reducing unemployment always required lower real wages, the red dots should consistently make upward sloping lines. The real picture, though, is more complicated.

As we can see, the early 2000s recovery and, arguably, the early 1980s recovery were associated with falling real wages. but in the early 1990s, employment recovered with constant real wages -- that's what the vertical line over on the left means. And in the two recessions of the 1970s, the recoveries combined falling unemployment with strongly rising real wages. If we look at other advanced countries, it's this last pattern we see most often. (I show some examples after the fold.) So while rising employment is sometimes accompanied by a falling real wage, it is clearly not true that, as Glasner claims, it necessarily must be.

This is an important question to get straight. There seems to be a certain convergence happening between progressive-liberal economists and neo-monetarists like Glasner on the desirability of higher inflation in general and nominal GDP targeting in particular. There's something to be said for this; inflation is the course of least resistance to cancel the debts. But we in the party of movement can't support this idea or make it part of a broader popular economic program if it's really a stalking horse for lower wages.

Fortunately, the macroeconomic benefits of a rising price level don't depend on a falling real wage.

More broadly, the idea that reducing unemployment necessarily means reducing wages doesn't hold up. It's wrong empirically, and it involves a basic misunderstanding of what's going on in recessions.

Yes, labor is idle in a recession, but does that mean its price, the wage, is too high? There is also more excess capacity in the capital stock in a recession; by the same logic, that would mean profits are too high. Real estate vacancy rates are high in a recession, so rents must also be too high. In fact, every factor of production is underutilized in recessions, but it's logically impossible for the relative price of all factors to be too high. A shortfall in demand for output as a whole (or excess demand for the means of payment, if you're a monetarist) doesn't tell us anything about whether relative prices are out of line, or in which direction. If we were seeing technological unemployment -- people thrown out of work by the adoption of more capital-intensive forms of production -- then there might be something to the statement that "unemployment ... implies that real wages are, in some sense, too high." But that's not what we see in recessions at all.

Glasner is hardly the only one who thinks that unemployment must somehow involve excessive wages. If he were, he'd hardly be worth arguing with. It's a common view today, and it was even more common before World War II. Glasner quotes Mises (yikes!), but Schumpeter said the same thing. More interestingly, so did Keynes. In Chapter Two of the General Theory, he announces that he is not challenging what he calls the first postulate of the classical theory of employment, that the wage is equal to the marginal product of labor. And he draws the same conclusion from this that Glasner does:

with a given organisation, equipment and technique, real wages and the volume of output (and hence of employment) are uniquely correlated, so that, in general, an increase in employment can only occur to the accompaniment of a decline in the rate of real wages. Thus I am not disputing this vital fact which the classical economists have (rightly) asserted... [that] the real wage earned by a unit of labour has a unique (inverse) correlation with the volume of employment. Thus if employment increases, then, in the short period, the reward per unit of labour in terms of wage-goods must, in general, decline... This is simply the obverse of the familiar proposition that industry is normally working subject to decreasing returns... So long, indeed, as this proposition holds, any means of increasing employment must lead at the same time to a diminution of the marginal product and hence of the rate of wages measured in terms of this product.So, wait, if Keynes says it then it can't be a basic misunderstanding of the principle of aggregate demand, can it? Well, here's where things get interesting.

Keynes didn't participate much in the academic discussions following the The General Theory; the last decade of his life was taken up with practical policy work. (As Hyman Minsky observed, this may be one reason why many of his more profound ideas never made into postwar Keynesianism.) But he take part in a discussion in the pages of the Quarterly Journal of Economics, in which the "most important" contribution, per Keynes, was from Jacob Viner, who zeroed in on exactly this question. Viner:

Keynes' reasoning points obviously to the superiority of inflationary remedies for unemployment over money-wage reductions. ... there would be a constant race between the printing press and the business agents of the trade unions, with the problem of unemployment largely solved if the printing press could maintain a constant lead... [But] Keynes follows the classical doctrine too closely when he concedes that "an increase in employment can only occur to the accompaniment of a decline in the rate of real wages." This conclusion results from too unqualified an application of law-of-diminishing-returns analysis, and needs to be modified for cyclical unemployment... If a plant geared to work at say 80 per cent of rated capacity is being operated at say only 30 per cent, both the per capita and the marginal output of labor may well be lower at the low rate of operations than at the higher rate, the law of diminishing returns notwithstanding. There is the further empirical consideration that if employers operate in their wage policy in accordance with marginal cost analysis, it is done only imperfectly and unconsciously...Viner makes two key points here: First, it is not necessarily the case that the marginal product of labor declines with output, especially in a recession or depression when businesses are producing well below capacity. And second, the assumption that wages are equal to marginal product is not a safe one. A third criticism came from Kalecki, that under imperfect competition firms would not set price equal to marginal cost but at some markup above it, a markup that will vary over the course of the business cycle. Keynes fully agreed that all three criticisms -- along with some others, which seem less central to me -- were correct, and that the first classical postulate was no better grounded than the second. In what I believe was his last substantive economic publication, a 1939 article in the Economic Journal, he returned to the question, showing that it was not true empirically that real wage fall when employment rises and exploring why he and other economists had gotten this wrong. The claim that higher employment must be accommpanied by a lower real wage, he wrote, "is the portion of my book which most needs to be revised." Indeed, it was the only substantive modification of the argument of the General Theory that he made in his lifetime.

I bring all this up because -- well, partly just because I think it's interesting. But it's worth being reminded, how much of our current economic debate is recapitulating what people were figuring out in the 1930s. And it's interesting to see how just how seductive is the idea that high unemployment means that "real wages are, in some sense, too high." Even Keynes had to be talked out of it, even though it runs counter to the logic of his whole system, and even though there's no good theoretical or empirical reason to believe it's true.

Right, back to empirics. Here are a few more graphs, showing, like the US one above, unemployment on the vertical axis and real hourly wages on the horizontal. Data is from the OECD.

The first picture shows five Western European countries in the decade before the crisis. The important part is the left side; what you see there is that in all five countries unemployment fell sharply in the late 90s/early 2000s, even while real wages increased. In Belgium, for example, unemployment fell from 10 percent to a bit over six percent between 1996 and 2002, at the same time as real wages rose by close to 10 percent. The other four (and almost every country in the EU) show similar patterns.

The second one shows Korea. The 1997 Asian crisis is clearly visible here as the huge spike in unemployment in the middle of the graph. But what's relevant here is the way it seems to slope backward. That's because real wages fell along with employment in the crisis, and rose with employment in the recovery. Over the same period that unemployment comes back down from 8 to 4 percent, the real wage index rises from 70 to 80. This is the opposite of what we would expect in the Glasner story.

The third one shows Australia and New Zealand. Australia shows two periods of sharply falling unemployment -- one in the 1980s accompanied by flat wages (a vertical line) and one in the 1990s accompanied by rising wages. Of all these countries, only New Zealand's recoveries show a pattern of falling unemployment accompanied by falling real wages -- clearly after 1992, and for a quarter or two in 2000.

UPDATE: In comments, Will Boisvert calls the graphs above the worst he's ever seen. OK!

So, here is the same data presented in a hopefully more legible way. The red line is unemployment, the blue line is the real hourly wage. The key question is, when the red line is falling from a peak, is the blue line falling too, or at least decelerating? And the answer, as above, is: Sometimes, but not usually. There is nothing dishonest in the claim that, in a recession, unemployment can be reduced without a decline in the real wage.

http://economistsview.typepad.com/economistsview/2009/12/on-the-consequences-of-nominal-wage-flexibility.html

ReplyDeleteI suppose that I'm stating something obvious, however: wages are both a component of the costs of production and a component of demand. We are in a slack-of-demand crisis.

ReplyDeleteTo say that lower wages would increase employment is to say that a fall in wages would impact more the costs of production than the aggregate demand; I can't see how could this happen in western economies.

This is a good post, but the graphs really suck. They look like a two-year-old's squiggles; it's virtually impossible to extract useful information from them, even with the explanatory paragraphs telling you what to look for. In fact, this is the worst visual display of quantitative information I have ever seen. (Here's a hint: if you need long paragraphs to explain your graph, your graph sucks.) Is this a standard format, and if so, who invented it and where is his homeworld?

ReplyDeletejch-

ReplyDeleteThanks. I hadn't seen that Becker was part of the lower-wages brigade.

RL-

Right. Keynes' argument in the GT is a bit different. His point is that we think prices are set as a markup over marginal costs, and marginal costs consist basically of wages, so to a first approximation changes in the money wage lead to a proportional change in the price level and leave the real wage unchanged. This is Keynes' explanation for why convincing workers to accept lower wages is not a solution to unemployment, despite the fact (as he believed then) that if unemployment were to fall, real wages would necessarily be lower. As I say, he subsequently rejected this second idea. But there's no logical contradiction in principle between the statements that output is constrained by demand, and that higher output would imply a lower real wage, though only the first one is generally true.

WB-

I'm certainly not the first person to draw graphs like these, showing a system moving through a state space. I think it can be a very efficient way of showing the relationship between two variables. But I suppose you're right that a graph is like a joke: If you have to explain why it's good, it's no good. OK, I'm adding some more conventional graphs showing the same thing.

My 2 cents: I thought this was pretty much settled. The evidence for anti-cyclical real wages is pretty slim; they are a-cyclical or pro-cyclical. There is a good survey paper in the JEL in the mid 90s by Katharine Abraham I think. The only exception is that some studies that use a real product wage definition (arguably superior) find some support for the marginal productivity theory. Am I out of date?

ReplyDeleteI think you're right.

ReplyDeleteOne of the things that's striking about this, is it's an example of how much of economic debate right now is about things that one would think would be settled questions.

... on the other hand, the difference between the real wage deflated by the CPI and the product wage is interesting. As I'm sure you know, there are several papers on the cyclical profit squeeze (by Erdogan Bakir, David Kotz, etc.) that talk about this. They point out that even though the real wage has been basically constant over recent business cycles,the wage share has still tended to rise in expansions and fall in recessions, because of the cyclical movement of the CPI relative to the GDP deflator. But that's again a story about pro-cyclical wages, and it has nothing to do with marginal productivity.

Also, it seems to me that if you take Okun's law seriously, you should expect marginal productivity of labor to move procyclically, at least around recessions. If businesses hoard labor, or simply can't adjust employment levels quickly, shouldn't the marginal product of labor be lowest at the bottom of recessions, when they have the most "extra" workers?

@ Josh,

ReplyDeleteThe new graphs are much better.

But I’d like to push back a little against the whole cult of visual display of quantitative information.

I know that’s all the rage these days, what with computer graphics and everything. We’re taught that we have to format information as pretty graphs and pictures, or better yet animated videos, in order for it to make an impression on people, especially kids.

But I think that’s not true as a general proposition. In most instances, conveying information through language and number symbols is a far more concise, evocative and compelling mode of communication than drawing pictures. Try conveying the following information, using only pictures with no words or numbers:

--“Four-score and seven years ago today, our fathers brought forth upon this continent a new nation, conceived in liberty…” yada yada.

Would an audience, just looking at your pictures, reliably and precisely return the ideas conveyed in that verbal-numeric statement? Which communication system would take more time, effort and resources to convey the information?

In the case of this post, I think you should have foregone graphics altogether. A tabular presentation of numerical figures judiciously selected from historical examples might have been more concise and easier to compare. Or simply formatting the information as verbal-numeric narrative, as you did anyway to explain the graphs: Just a compact series of sentences saying “in this country during this recovery, unemployment dropped from here to there while wages rose from there to here.” You couldn’t fit all the data points on your graphs into your narrative—but that would force you to focus on the most telling ones, which might add to the concision and power of your presentation.

People should think hard before resorting to graphs. Most of the time, a word is worth a thousand pictures.

I don't agree with the statement:

ReplyDelete"In fact, every factor of production is underutilized in recessions, but it's logically impossible for the relative price of all factors to be too high."

Is it not the basis of most theories of deficient AD that it is sticky prices at a time of increased demand for money that cause recessions? In this case then the relative prices of all factors could indeed be too high. I think that the main tenet of the market monetarists is that fed should further inflate the money supply precisely because they believe this will avoid the necessity of a fall in the general price level.

I'm a physicist and think those graphs are great. We call them phase space plots. And yes your plots are noisy. We like noise too: all real data have noise. Data, yummy.

ReplyDelete@ Raymond Lutz,

ReplyDeleteWhat's great about the graphs? And why do you love noise? Just because it feels more authentic, more "real"?

Is it not the basis of most theories of deficient AD that it is sticky prices at a time of increased demand for money that cause recessions?

ReplyDeleteThis is a feature of SOME theories of deficient demand. But even if you accept the monetarist claim (which I don't) that you have a recession because the the price level is too high for the given fixed stock of money, that is different from saying that relative price are wrong. A fall in the price level would not change real wages.

Raymond,

ReplyDeletePhase space, right. Thanks! It's great to have a real scientist reading this stuff.