You know, there's a fundamental parallel between what's wrong with Krugman's takes on monetary policy and on trade.

In the first case, his argument is that the interest rate (a price, administered to be sure) would normally equilibrate savings and investment at something like full employment. It's the barrier to that price's adjustment in the form of the zero lower bound that causes income to adjust instead, leading to the Great Recession (and the need for fiscal policy). Similarly trade flows are normally equilibrated by the adjustment of the exchange rate, a price. It's barriers to that price's adjustment, in the form of the Euro and the RMB-dollar peg, that cause income to adjust instead, leading to austerity in peripheral Europe and unemployment in the United States.

From a Post Keynesian perspective, these are kludges that get good conclusions from bad premises.

From a Post Keynesian (or for that matter Keynesian straight-up) perspective, flexible interest rates and exchange rates have never reliably delivered macroeconomic balance. Income adjustments aren't a once-in-a-lifetime feature of the current conjuncture, they're a routine and central feature of capitalism.

New Keynesian economists like Krugman can see that macroeconomic reality today doesn't conform to the textbook, where prices smoothly converging to market-clearing levels. (Well, maybe to the 1978 edition.) But they're not going to throw the textbook away, so the departures are explained as a series of ad hoc special cases. And so the textbook has a way of sneaking back in whenever their attention is elsewhere. That's why Krugman insists something big changed when the federal funds rate hit zero, even though the federal funds rate has been more or less disconnected from most longer rates for a decade or more. And that's why he insists that the Asian crisis countries were better off than Greece, etc. because they could devalue their currencies instead of resorting to austerity, when it seems clear that devaluations contributed little to Asian countries' improved current account balances after 1997; they drastically cut domestic spending, just as peripheral Europe is being forced to. When he's looking right at a non-price adjustment mechanism, he can see it; but wherever he's not looking, he assumes that prices are doing their thing.

Or at least that's how it looks to me.

Saturday, April 30, 2011

Monday, April 25, 2011

What's Good Enough for GE Is Good Enough for America

[Originally posted at New Deal 2.0.]

S&P's threat to downgrade the US government's credit rating has been dismissed by economist-bloggers as a political intervention by bondowners and compared to "adorable children wearing their underpants outside their trousers." As far as the chances of the US someday defaulting on its debt go, the announcement has zero informational value.

Still, it's true that federal debt held by the public has reached 60 percent of GDP, while tax revenues remain around 20 percent of GDP. 60 percent of GDP is a lot! And double, nearly triple, tax revenue! What would we call a company with outstanding debt double or even triple its revenues, and expected to keep the highest bond rating?

We could call it General Electric.

Still, it's true that federal debt held by the public has reached 60 percent of GDP, while tax revenues remain around 20 percent of GDP. 60 percent of GDP is a lot! And double, nearly triple, tax revenue! What would we call a company with outstanding debt double or even triple its revenues, and expected to keep the highest bond rating?

We could call it General Electric.

As recently as 2007, GE had an S&P rating of AAA with outstanding debt at over three time revenues. Or we could call it the Tennessee Valley Authority; TVA managed outstanding debt of 3.9 times revenue in the late '90s (it's since come down a bit), and S&P never downgraded its bond rating from AAA. Or, we could call it Hydro Quebec, with debt of over 4.5 times revenues (altho, admittedly, its S&P rating is only A+). Or the natural gas and energy supplier TransCanada, with debt equal to 2.2 time revenues and an A rating from S&P. Even Transocean, which operated the Deepwater Horizon rig for BP, managed an A- rating prior to the spill, with a debt-revenue ratio similar to what the federal government has now.

Now, it's perfectly sensible for a big utility, with its high proportion of long-lived fixed capital and stable revenue streams, to carry a lot of debt. If I ran Hydro Quebec (and converting the company to a worker- and consumer-owned cooperative wasn't an option), I'd take on a lot of debt too. But here's the point. If the question is, what if the government had to fund itself like a private business, the answer isn't necessarily that it would do anything different from what it's doing now.

In the real world, of course, there are lots of differences between the government of the United States and a private business. The federal government issues the currency that its debt is denominated in. It has effectively unlimited authority to increase taxes on the private sector. And its liabilities are the most important store of value and means of payment for the private sector. (When Alan Greenspan said that the financial system would have a real problem without holdings of federal debt, he may have been arguing in bad faith, but he wasn't wrong.) And of course, the US government is responsible for output and employment in the economy as a whole, and not just for its own balance sheet. All these differences mean that it makes sense for the US government to carry more debt than a private business. If GE or Transocean are safe bets for lenders with debt of two or three times revenue, then the federal government must be ultra ultra safe. Which, interestingly enough, is just what the bond market says.

So perhaps we can get away from the "oooh, that's a really big number!" school of analysis of federal borrowing. And instead ask what levels of federal deficit and outstanding debt are most compatible with economic growth and financial stability. For the foreseeable future, I'd suggest, the answer has a lot more to do with the role of government spending in aggregate demand, and with government debt as a risk-free asset for the private sector, than with the level of debt that's "sustainable". Because if you think there are more states of the world where TVA or GE make their payments to bondholders than where the US government does, you must be smoking something from S&P's private stash.

UPDATE: This excellent post from Mike Konczal makes the same point more systematically.

Now, it's perfectly sensible for a big utility, with its high proportion of long-lived fixed capital and stable revenue streams, to carry a lot of debt. If I ran Hydro Quebec (and converting the company to a worker- and consumer-owned cooperative wasn't an option), I'd take on a lot of debt too. But here's the point. If the question is, what if the government had to fund itself like a private business, the answer isn't necessarily that it would do anything different from what it's doing now.

In the real world, of course, there are lots of differences between the government of the United States and a private business. The federal government issues the currency that its debt is denominated in. It has effectively unlimited authority to increase taxes on the private sector. And its liabilities are the most important store of value and means of payment for the private sector. (When Alan Greenspan said that the financial system would have a real problem without holdings of federal debt, he may have been arguing in bad faith, but he wasn't wrong.) And of course, the US government is responsible for output and employment in the economy as a whole, and not just for its own balance sheet. All these differences mean that it makes sense for the US government to carry more debt than a private business. If GE or Transocean are safe bets for lenders with debt of two or three times revenue, then the federal government must be ultra ultra safe. Which, interestingly enough, is just what the bond market says.

So perhaps we can get away from the "oooh, that's a really big number!" school of analysis of federal borrowing. And instead ask what levels of federal deficit and outstanding debt are most compatible with economic growth and financial stability. For the foreseeable future, I'd suggest, the answer has a lot more to do with the role of government spending in aggregate demand, and with government debt as a risk-free asset for the private sector, than with the level of debt that's "sustainable". Because if you think there are more states of the world where TVA or GE make their payments to bondholders than where the US government does, you must be smoking something from S&P's private stash.

UPDATE: This excellent post from Mike Konczal makes the same point more systematically.

Sunday, April 24, 2011

Nelson Algren, Asshole

Never Come Morning is my favorite American novel, full stop. But this here is a remarkably bitchy memoir/parody.

Mailer as Norman Manlifellow, "the boyish author of The Elk Paddock or Look Ma, My Fly Is Open? Ok, heavy-handed but ok. Alfred Paperfish must be Edmund Wilson, and his wife with "just time for a quickie" is Mary McCarthy. Leon Urine, author of The Whole World Looks Jewish When You're in Love, Roth maybe? Ginny Ginstruck? I don't know, an editor or agent, a woman anyway, certainly someone he didn't like. But Baldwin as Giovanni Johnson, lisping in cliche Gay and singing Dis train don't carry no gamblers, that's not funny, sorry, no. The parts that are genuinely respectful only make the nasty bits nastier. And a speech about how Negroes have been "'knocked down, strung up, run over, banjaxed, castrated, jillflirted, stomped, harassed, jeered at, vilified, despised, warped' -- he paused to change fingers, as he tires easily..." No, again not funny. Black men really were castrated. It isn't funny even if you juxtapose it with a couple nonsense words.

Algren, beautiful writer, bitter man.

Mailer as Norman Manlifellow, "the boyish author of The Elk Paddock or Look Ma, My Fly Is Open? Ok, heavy-handed but ok. Alfred Paperfish must be Edmund Wilson, and his wife with "just time for a quickie" is Mary McCarthy. Leon Urine, author of The Whole World Looks Jewish When You're in Love, Roth maybe? Ginny Ginstruck? I don't know, an editor or agent, a woman anyway, certainly someone he didn't like. But Baldwin as Giovanni Johnson, lisping in cliche Gay and singing Dis train don't carry no gamblers, that's not funny, sorry, no. The parts that are genuinely respectful only make the nasty bits nastier. And a speech about how Negroes have been "'knocked down, strung up, run over, banjaxed, castrated, jillflirted, stomped, harassed, jeered at, vilified, despised, warped' -- he paused to change fingers, as he tires easily..." No, again not funny. Black men really were castrated. It isn't funny even if you juxtapose it with a couple nonsense words.

Algren, beautiful writer, bitter man.

Tuesday, April 19, 2011

Selfish Masters, Selfless Servants

Via Mike the Mad Biologist, a Confucian parable for the financial crisis:

Greenwood is talking about the "corporation as polis." But the same point applies to the polis as polis.

It may not be the benevolence that makes the butcher, baker or brewer hand over the beef, bread or beer. But it is benevolence-- or at least something other than self-interest -- that ensures that it's not full of E. coli. And if you say, well, it's just their self-interest in avoiding the penalties of the law, that begs the question of why the authorities enforce the law. Or as Hume famously observed,

All of which is another way of saying that, despite the fantasies of libertarians, and cynics, that it's self-interest all the way down, we can't dispense with intrinsic motivation, analytically or in practice.

UPDATE: Added Groys quote. Had intended to include it in the original post, but I'd lent the book to someone...

Mencius replied, "Why must your Majesty use that word 'profit?' What I am provided with, are counsels to benevolence and righteousness, and these are my only topics.Indeed, there are deep contradictions hidden in that word "profit." Reminds me of a classic article on corporate governance, Bruce Greenwood's Enronitis: Why Good Corporations Go Bad.

"If your Majesty say, 'What is to be done to profit my kingdom?' the great officers will say, 'What is to be done to profit our families?' and the inferior officers and the common people will say, 'What is to be done to profit our persons?' Superiors and inferiors will try to snatch this profit the one from the other, and the kingdom will be endangered....

The Enron problem is ... the predictable result of too strong of a share-centered view of the public corporation... Corporate law demands that managers simultaneously be selfless servants and selfish masters. On the one hand, it directs managers to be faithful agents, setting aside their own interests entirely in order to act only on behalf of their principals, the shares. On the other hand, in the service of this extreme altruism, they must ruthlessly exploit everyone around them, projecting on to the shares an extreme selfishness that takes no account of any interests but the shares themselves. Having maximally exploited their fellow human corporate participants, managers are then expected to selflessly hand over their gains...Something like Enronitis was clearly involved in the financial crisis. Indeed, some of the most famous controversies around the crisis hinge precisely on disputes about whether a transaction was between the parties linked by a fiduciary duty, or was an arm's-length one where predatory behavior was expected, and even a moral duty. You can get yourself out of legal trouble, as Goldman has in the case of the Paulson trade, by establishing that you were on the war-of-all-against-all side of the line; but obviously, a system where predatory and trust-based relationships are expected to exist side by side, or even to overlap, is not likely to be a sustainable one. (Of course if the goal of our rentier elite is simply to stripmine the postwar social compromise, then sustainability is moot.) Friedman's idea that a corporation's duty is "to make as much money as possible while conforming to the basic rules of the society" isn't coherent psychologically or logically, since it demands that management regard certain norms as absolutely binding and others as absolutely non-binding, without any reliable way of saying which is which.

Altruism and rationally self-interested exploitation are extreme and radically opposed positions, psychologically and politically. ... For managers, one easy resolution of these tensions is a simple, cynical selfishness in which managers see themselves as entitled, and perhaps even required, to exploit shareholders as ruthlessly as they understand the law to require them to exploit everyone else. ...

Internally, the share-centered paradigm is just as self-destructive. Corporations succeed because they are not markets and do not follow market norms of behavior. Rather, they operate under fiduciary norms as a matter of law and team norms as a matter of sociology. However, the share-centered paradigm of corporate law teaches managers to treat employees as outsiders and tools to corporate ends with no intrinsic value. Just as managers are unlikely to learn simultaneously to be selfish maximizers and selfless altruists, they are unlikely to be simultaneously cooperative team players and self-interested defectors. Thus, the share-centered view undermines the prerequisite to operating the firm in the interests of shareholders. ...

Managers constructing the firm as a tool to the end of share value maximization treat the people with whom they work as means, not ends. ...they learn as part of their ordinary life to break ordinary social solidarity. Learning to exploit ruthlessly is surprisingly difficult. ... But cynicism can be learned, and managers subjected to the powerful incentives of the share value maximization principle do eventually learn it. ... This training, however, surely creates cynics, not faithful agents. ... A manager whose lived experience is a pretense of selflessness (with respect to employees, customers and business partners) covering real disinterested exploitation (on behalf of shares) is unlikely to suddenly see himself as “in a position in which thought of self was to be renounced, however hard the abnegation” and voluntarily hand over these hard-won gains of competitive practice to his principal. If you can properly lie to your subordinates, why not lie to your superior as well? ... In the end, the cynicism of the share value maximization view must eat itself alive.

Greenwood is talking about the "corporation as polis." But the same point applies to the polis as polis.

It may not be the benevolence that makes the butcher, baker or brewer hand over the beef, bread or beer. But it is benevolence-- or at least something other than self-interest -- that ensures that it's not full of E. coli. And if you say, well, it's just their self-interest in avoiding the penalties of the law, that begs the question of why the authorities enforce the law. Or as Hume famously observed,

as FORCE is always on the side of the governed, the governors have nothing to support them but opinion. It is therefore, on opinion only that government is founded; and this maxim extends to the most despotic and most military governments, as well as to the most free and most popular. The soldan of EGYPT, or the emperor of ROME, might drive his harmless subjects, like brute beasts, against their sentiments and inclination: But he must, at least, have led his mamalukes, or prætorian bands, like men, by their opinion.Boris Groys develops a similar line of thought in The Communist Postscript:

The theory of Marxism-Lenisnism is ambivalent in its understanding of language, as it is in most matters. On the one hand, everyone who knows this theory has learnt that the dominant language is always the language of the dominant classes. On the other hand, they have learnt too that an idea that has gripped the masses becomes a material force, and that on this basis Marxism itself is (or will be) victorious because it is correct.This is a particular instance of Groys' broader argument about the inherent power of rational speech:

The listener or reader of an evident statement can of course willfully decide to contradict the compelling effect of this statement... But someone who adopts such a counter-evident position does not really believe it himself. Those who do not accept what is logically evident become internally divided, and this division weakens them in comparison to those who accept and affirm the evidence. The acceptance of logical evidence makes one stronger; to reject it, conversely, makes one weaker.Similarly, the decisionmaker who acts on norms consistently is stronger, in the long run, than the Enronitic manager whose honest service to "shareholder value" requires dishonest, strictly instrumental treatment of workers, customers, regulators, and the rest of humanity.

All of which is another way of saying that, despite the fantasies of libertarians, and cynics, that it's self-interest all the way down, we can't dispense with intrinsic motivation, analytically or in practice.

UPDATE: Added Groys quote. Had intended to include it in the original post, but I'd lent the book to someone...

Saturday, April 16, 2011

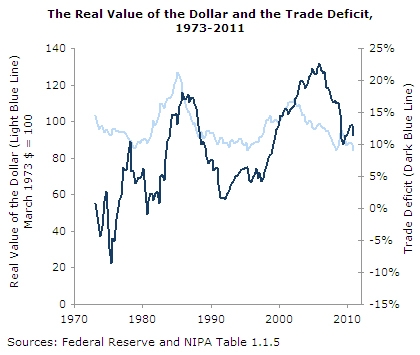

Do Prices Matter?

Do exchange rates drive trade flows? Yes, says Dean Baker David Rosnick. Prices matter:

Dean folks at CEPR would agree, that doesn't it mean it's what we actually see. You have to look at the evidence.

So what's the evidence on this point? Dean Rosnick offers a graph showing two big falls in the value of the dollar after peaks in the mid-80s and mid-2000s, and falls in the trade deficit a few years later, in the early 90s and late 2000s. Early 90s and late 2000s ... hm, what else was happening in those years? Oh, right, deep recessions. (The early 2000s recession was very mild.) Funny that the same guy who's constantly chastising economists for ignoring the growth and collapse of a huge housing bubble, when he turns to trade ... ignores a huge housing bubble.

Still, isn't the picture is basically consistent with the story that when the dollar declines, US imports get more expensive and fall, and US exports get cheaper and rise? Not necessarily:Dean's Rosnick's graph doesn't show imports and exports separately. And when we separate them out, we see something funny.

In a world where trade flows were mainly governed by exchange rates, a country's imports and exports would show a negative correlation. After all, the same exchange-rate change that makes exports more expensive on world markets makes imports cheaper here, and vice versa. But that isn't what we see at all. Except in the 1980s (when the exchange rate clearly did matter, but not in the wayDean Rosnick supposes; see Robert Blecker) exports and imports very clearly move together. And it's not just a matter of a long-term rise in both imports and exports. Every period that saw a significant fall in imports -- 1980-1984; 2000-2002; 2007-2009 -- saw a large fall in exports as well. This is simply not what happens in a world where prices (are the main things that) matter.

(This discrepancy between real-world trade patterns and the textbook vision applies to almost all industrialized countries, and always has. It was noticed long ago by Robert Triffin, who brought it up to argue that movements in relative price levels did not govern trade patterns under the gold standard, as Ricardo and his successors had claimed. But it is just a strong counterargument to today's conventional wisdom that exchange rates govern trade.)

So if changes in exchange rates don't drive trade, what does? Lots of things, many of them no doubt hard to measure, or to influence through policy. But one obvious candidate is changes in incomes. One of the big advances of the first generation of Keynesian economists -- people like Triffin, and especially Joan Robinson -- was to show how, just as prices (the wage and interest rates) fail to equilibrate the domestic economy, leaving aggregate income to adjust, relative prices internationally don't equilibrate the global economy, leaving output or growth rates to adjust. In the short run, business cycle-type fluctuations reliably involve changes in investment and consumer-durable purchases larger disproportionate to the change in output as a whole; given the mix of traded and non-trade goods for most countries, this creates an allometry in which short-run changes in output are accompanied by even larger short-run changes in imports and exports. For a country that runs a trade deficit in "normal" times, this means that recessions are reliably associated with smaller deficits and booms with larger ones. In the long run, there is also a reliable tendency for increments to income to involve demand for a changing mix of goods, with a greater share of demand falling on "leading sectors," historically manufactured goods. (The flipside of this is Engels' law, which states that the share of income spent on food falls as income rises.) Given that both a country's mix of industries and its trade partners are relatively fixed, this creates a stable relationship between relative growth rates and trade balance movements. Neither of these channels is perfectly reliable, by any means -- and the whole point of the industrial policy is to circumvent the second one -- but they are still much stronger influences on trade flows than exchange rates (or other relative prices) are.

So with that in mind, let's look at another version of the graph. This one shows the year-over-year change in the trade balance as a share of GDP, the same change as predicted by an OLS regression on total GDP growth over the past three years, and as predicted by the change in the value of the dollar over the past three years. [1]

It will be legible if you click it.

It will be legible if you click it.

Not surprisingly, neither prediction gives a terribly close fit. But qualitatively, at least, the predictions based on GDP do a reasonable job: They capture every major worsening and improvement in the trade balance. True, they under-predict the improvement in the trade balance in the later 80s -- the Plaza Accords mattered -- but it's clear that if you knew the rate of GDP growth over the next three years, you could make a reasonably reliable prediction about the the behavior of the trade balance. Knowing the change in the value of the dollar, on the other hand,wouldn't help you much at all. (And just to be clear, this isn't about the particular choice of three years. Two years and four years look roughly similar, and at a one-year horizon exchange rates aren't predictive at all.)

Here's another presentation of the same data, a scatterplot comparing the three-year change in the trade balance to the three-year growth of GDP (blue, left axis) and three-year change in the exchange rate (red, right axis). Again, while the correlation is fairly loose for both, it's clearly tighter for GDP. All the periods of strongest improvement in the trade balance are associated with weak GDP growth, and vice versa; similarly all the periods of strong GDP growth are associated with worsening of the trade balance, and vice versa. There's no such consistent association for the trade balance and changes in the exchange rate.

The fit could be improved by using some measure of disposable income -- ideally adjusted for wealth effects -- in place of GDP, and by using some better measure of relative prices in place of the exchange-rate index -- altho there's some controversy about what that better measure would be. And theoretically, instead of just the three-year change, you should use the individual lags.

Still, the takeaway, if you're a policymaker, is clear. If you want to improve the trade balance, slower growth is the way to go. And if you want to boost growth, you probably are going to have to ignore the trade balance. Personally, I want door number two. I assumeDean Rosnick doesn't want door one. But what I'm not at all sure about, is what concrete evidence makes him think that exchange-rate policy opens up a third door.

What happens to the economy as the dollar falls? ...Over time, Americans notice that British goods have become more expensive in comparison to domestically produced goods. In other words, the price of U.S.-made sweaters becomes cheaper relative to the price of sweaters imported from Britain. This will lead us to buy fewer sweaters from Britain and more domestically manufactured sweaters.

At the same time, the British notice that American goods have become relatively inexpensive in comparison to goods made at home. This means it takes fewer pounds to buy a sweater made in the United States, so the British will buy more sweaters made in the United States and fewer of their domestically manufactured sweaters.Indeed it's not. Changes in prices induce changes in transaction volumes that smoothly restore equilibrium, is the first article of the economist's catechism. But how much a given volume responds to a given price change, and whether the response is reliable and strong enough to make the resulting equilibrium relevant to real economies, are empirical questions. You could tell a similar parable about an increase in the minimum wage leading to a lower demand for low-wage labor, but as I'm sure

While American producers notice the increased demand for their exports, allowing them to raise their prices somewhat and still sell more than they had before the dollar fell. Similarly, for British exporters to continue selling they must lower prices.

Thus, as everyone eventually adjusts to the fall in the dollar, the trade deficit shrinks. This is not new economics by any stretch...

So what's the evidence on this point?

{kind=link}

Still, isn't the picture is basically consistent with the story that when the dollar declines, US imports get more expensive and fall, and US exports get cheaper and rise? Not necessarily:

Click the graph to make it legible.

In a world where trade flows were mainly governed by exchange rates, a country's imports and exports would show a negative correlation. After all, the same exchange-rate change that makes exports more expensive on world markets makes imports cheaper here, and vice versa. But that isn't what we see at all. Except in the 1980s (when the exchange rate clearly did matter, but not in the way

(This discrepancy between real-world trade patterns and the textbook vision applies to almost all industrialized countries, and always has. It was noticed long ago by Robert Triffin, who brought it up to argue that movements in relative price levels did not govern trade patterns under the gold standard, as Ricardo and his successors had claimed. But it is just a strong counterargument to today's conventional wisdom that exchange rates govern trade.)

So if changes in exchange rates don't drive trade, what does? Lots of things, many of them no doubt hard to measure, or to influence through policy. But one obvious candidate is changes in incomes. One of the big advances of the first generation of Keynesian economists -- people like Triffin, and especially Joan Robinson -- was to show how, just as prices (the wage and interest rates) fail to equilibrate the domestic economy, leaving aggregate income to adjust, relative prices internationally don't equilibrate the global economy, leaving output or growth rates to adjust. In the short run, business cycle-type fluctuations reliably involve changes in investment and consumer-durable purchases larger disproportionate to the change in output as a whole; given the mix of traded and non-trade goods for most countries, this creates an allometry in which short-run changes in output are accompanied by even larger short-run changes in imports and exports. For a country that runs a trade deficit in "normal" times, this means that recessions are reliably associated with smaller deficits and booms with larger ones. In the long run, there is also a reliable tendency for increments to income to involve demand for a changing mix of goods, with a greater share of demand falling on "leading sectors," historically manufactured goods. (The flipside of this is Engels' law, which states that the share of income spent on food falls as income rises.) Given that both a country's mix of industries and its trade partners are relatively fixed, this creates a stable relationship between relative growth rates and trade balance movements. Neither of these channels is perfectly reliable, by any means -- and the whole point of the industrial policy is to circumvent the second one -- but they are still much stronger influences on trade flows than exchange rates (or other relative prices) are.

So with that in mind, let's look at another version of the graph. This one shows the year-over-year change in the trade balance as a share of GDP, the same change as predicted by an OLS regression on total GDP growth over the past three years, and as predicted by the change in the value of the dollar over the past three years. [1]

It will be legible if you click it.

It will be legible if you click it.Not surprisingly, neither prediction gives a terribly close fit. But qualitatively, at least, the predictions based on GDP do a reasonable job: They capture every major worsening and improvement in the trade balance. True, they under-predict the improvement in the trade balance in the later 80s -- the Plaza Accords mattered -- but it's clear that if you knew the rate of GDP growth over the next three years, you could make a reasonably reliable prediction about the the behavior of the trade balance. Knowing the change in the value of the dollar, on the other hand,wouldn't help you much at all. (And just to be clear, this isn't about the particular choice of three years. Two years and four years look roughly similar, and at a one-year horizon exchange rates aren't predictive at all.)

Here's another presentation of the same data, a scatterplot comparing the three-year change in the trade balance to the three-year growth of GDP (blue, left axis) and three-year change in the exchange rate (red, right axis). Again, while the correlation is fairly loose for both, it's clearly tighter for GDP. All the periods of strongest improvement in the trade balance are associated with weak GDP growth, and vice versa; similarly all the periods of strong GDP growth are associated with worsening of the trade balance, and vice versa. There's no such consistent association for the trade balance and changes in the exchange rate.

If you want to be able to read the graph, you should click it.

The fit could be improved by using some measure of disposable income -- ideally adjusted for wealth effects -- in place of GDP, and by using some better measure of relative prices in place of the exchange-rate index -- altho there's some controversy about what that better measure would be. And theoretically, instead of just the three-year change, you should use the individual lags.

Still, the takeaway, if you're a policymaker, is clear. If you want to improve the trade balance, slower growth is the way to go. And if you want to boost growth, you probably are going to have to ignore the trade balance. Personally, I want door number two. I assume

[1] Technicalities. I separately regressed the changes in imports and exports (as a percent of GDP) over three years earlier, on the percentage change over the same period in GDP and in the Fed's trade-weighted major-partners dollar index, respectively. It's all quarterly data, downloaded from FRED. The graphs shows the predicted values from the two regressions. This is admittedly crude, but I would argue that the more sophisticated approaches are in some respects less appropriate for the specific question being addressed here. For example, suppose hypothetically that a currency devaluation really did tend to improve the trade balance, but that it also tended to raise GDP growth, raising imports and offsetting the initial improvement. From an analytic standpoint, it might be appropriate to correct for the induced GDP change to get a better estimate of the pure exchange-rate effect. But from a policy perspective, the offsetting growth-imports effect has to be taken into account in evaluating the effects of a devaluation, just as much as the initial trade-balance improvement. Maybe we should say: Academics are interested in partial derivatives, policymakers in total derivatives?

EDIT: Oops! How did I not notice that this article was by somebody named David Rosnick, not Dean Baker? Makes me feel a bit better -- I know Dean does share this article's basic view of trade and the dollar, but I would hope his take would be a little less dependent on textbook syllogisms, and a little more attentive to actual patterns of trade. Clothing from the UK is hardly representative of US imports; to the extent we do import any, it's like to be high-end branded stuff that is particularly price-inelastic.

Tuesday, April 12, 2011

FIRE in the Whole

Maybe the most interesting paper at this past weekend's shindig at Bretton Woods was Duncan Foley's. [1] He argues, essentially, that it's wrong to include finance, real estate and insurance (FIRE) in measures of output. Excluding FIRE (and some other services) isn't just conceptually more correct, it has practical implications -- the big one being that an Okun's law-type relationship between employment and output is more stable if we define output to exclude FIRE and other sectors where value-added can't be directly measured.

It's a provocative argument. He's certainly right that the definition of GDP involves some more or less arbitrary choices about what is included in final output. (The New York Fed had a nice piece on this, a couple years ago, which was the subject of the one of the first posts on this humble blog.) However, I can't help thinking that Foley is wrong on a couple key points. Specifically:

It seems to me that there is a valid & important point here, but Foley doesn't quite make it. The key thing is that there is no way of measuring price changes in FIRE. That's what he should have said in place of the paragraph quoted above. The convention used in the national accounts is that the price of FIRE services rises at the same rate as the price level as a whole, so changes in nominal FIRE incomes relative total nominal income represent changes in FIRE's share of total output. But you could just as consistently say that FIRE output grows at the same level as output as a whole, and deviations in nominal FIRE expenditure represent relative changes in FIRE prices. [2] There's no empirical way of distinguishing these cases, it really is a convention. Doing it the second way would imply lower real GDP and higher inflation. I think this is the logically consistent version of Foley's argument. And it would motivate the same empirical points about Okun's Law, etc.

There's another argument, tho, which I don't quite have a handle on. Which is, what are the implications of considering FIRE services intermediate inputs rather than part of final output? If a firm pays more money to a software firm, that's considered investment spending and final output is corresponding higher. If a firm pays more money to a marketing firm, that's considered an intermediate good and final output is no higher, instead measured productivity is lower. I think that FIRE services provided to firms are considered intermediate goods, i.e. are already treated the way Foley thinks they should be. But I'm not sure. And there's still the problem of FIRE services purchased by households. There's no category of intermediate-goods purchases by households in the national accounts; any household expenditure is either consumption or investment, so contributes to GDP. This is a real issue, but again it's not unique to FIRE; e.g. why are costs associated with commuting considered part of final output when if a business provides transportation for its employees, that's an intermediate good?

He raises a third question, about the possibility that measured FIRE outputs includes asset transfers or capital gains. There is serious potential slippage between sale of financial services (part or GDP, conceptually) and sale of financial assets (not part of GDP).

Finally, it would be helpful to distinguish between services where measuring output is practically difficult but conceptually straightforward, and FIRE proper (and maybe insurance goes in the previous category). It seems clear that capital allocation as such should not be considered as part of final output. Whatever contribution it makes to total output (modulo the deep problems with measuring aggregate output at all) must come from higher productivity in the real economy. The problem is, there's no real way to separate the "normal service" component of FIRE from the capital-allocation and representation-of-capitalist-interests (per Dumenil and Levy; or you could say rent-extraction) components.

But whatever the flaws of the paper, it's pointing to a very important & profound set of issues. We can't bypass the conceptual challenges of GDP, as Matt Yglesias (like lots of other people) imagines, with the simple assertion that labor is productive if it produces something that people are willing to pay for. Producing a consistent series for GDP still requires deliberate decisions about how to measure price changes, and how to distinguish intermediate goods from final output. Foley is absolutely right to call attention to these problems, that most social scientists are happy to sweep under the rug [3]; he's right that they're especially acute in the case of FIRE; and I think he's probably right to say that to solve them we would do well to return to the productive/unproductive distinction of the classical economists.

[1] I wasn't there, but a comrade who was thought so. And he seems to be right, based on the papers they've got up on the website.

[2] Or you could say that FIRE output is fixed (perhaps at 0), and all changes in nominal FIRE output represents price changes. Again, this problem can't be resolved empirically, nor does it go away simply because you adopt a utility-based view of value.

[3] Bob Fitch had some smart things to say about the need to distinguish productive and unproductive labor.

It's a provocative argument. He's certainly right that the definition of GDP involves some more or less arbitrary choices about what is included in final output. (The New York Fed had a nice piece on this, a couple years ago, which was the subject of the one of the first posts on this humble blog.) However, I can't help thinking that Foley is wrong on a couple key points. Specifically:

While in other industries such as Manufacturing (MFG) there are independent measures of the value added by the industry and the incomes generated by it (value added being measurable as the difference between sales revenue and costs of purchased inputs excluding new investment and labor), there is no independent measure of value added in the FIRE and similar industries mentioned above. The national accounts “impute” value added in these industries to make it equal to the incomes (wages and profits) generated. Thus when Apple Computer or General Electric pay a bonus to their executives, GDP does not change (since value added does not change–the bonus increases compensation of employees and decreases retained earnings), but when Goldman-Sachs pays a bonus to its executives, GDP increases by the same amount.This seems confused on a couple of points. First, unless I'm mistaken, value-added in FIRE is calculated exactly in the way he describes -- sale price of output minus cost of inputs. (The problem arises with government, where there is no sale price.) Second, I'm pretty sure there is no difference in the way wages are treated -- total incomes in a sector always equal the total product of the sector, by definition. There is a question of whether executive bonuses are properly considered labor income or capital income, but that's orthogonal to the issues the paper raises, and is not unique to FIRE. In any case, it is definitely not correct to say that higher compensation implies lower earnings in non-FIRE but not in FIRE.

It seems to me that there is a valid & important point here, but Foley doesn't quite make it. The key thing is that there is no way of measuring price changes in FIRE. That's what he should have said in place of the paragraph quoted above. The convention used in the national accounts is that the price of FIRE services rises at the same rate as the price level as a whole, so changes in nominal FIRE incomes relative total nominal income represent changes in FIRE's share of total output. But you could just as consistently say that FIRE output grows at the same level as output as a whole, and deviations in nominal FIRE expenditure represent relative changes in FIRE prices. [2] There's no empirical way of distinguishing these cases, it really is a convention. Doing it the second way would imply lower real GDP and higher inflation. I think this is the logically consistent version of Foley's argument. And it would motivate the same empirical points about Okun's Law, etc.

There's another argument, tho, which I don't quite have a handle on. Which is, what are the implications of considering FIRE services intermediate inputs rather than part of final output? If a firm pays more money to a software firm, that's considered investment spending and final output is corresponding higher. If a firm pays more money to a marketing firm, that's considered an intermediate good and final output is no higher, instead measured productivity is lower. I think that FIRE services provided to firms are considered intermediate goods, i.e. are already treated the way Foley thinks they should be. But I'm not sure. And there's still the problem of FIRE services purchased by households. There's no category of intermediate-goods purchases by households in the national accounts; any household expenditure is either consumption or investment, so contributes to GDP. This is a real issue, but again it's not unique to FIRE; e.g. why are costs associated with commuting considered part of final output when if a business provides transportation for its employees, that's an intermediate good?

He raises a third question, about the possibility that measured FIRE outputs includes asset transfers or capital gains. There is serious potential slippage between sale of financial services (part or GDP, conceptually) and sale of financial assets (not part of GDP).

Finally, it would be helpful to distinguish between services where measuring output is practically difficult but conceptually straightforward, and FIRE proper (and maybe insurance goes in the previous category). It seems clear that capital allocation as such should not be considered as part of final output. Whatever contribution it makes to total output (modulo the deep problems with measuring aggregate output at all) must come from higher productivity in the real economy. The problem is, there's no real way to separate the "normal service" component of FIRE from the capital-allocation and representation-of-capitalist-interests (per Dumenil and Levy; or you could say rent-extraction) components.

But whatever the flaws of the paper, it's pointing to a very important & profound set of issues. We can't bypass the conceptual challenges of GDP, as Matt Yglesias (like lots of other people) imagines, with the simple assertion that labor is productive if it produces something that people are willing to pay for. Producing a consistent series for GDP still requires deliberate decisions about how to measure price changes, and how to distinguish intermediate goods from final output. Foley is absolutely right to call attention to these problems, that most social scientists are happy to sweep under the rug [3]; he's right that they're especially acute in the case of FIRE; and I think he's probably right to say that to solve them we would do well to return to the productive/unproductive distinction of the classical economists.

[1] I wasn't there, but a comrade who was thought so. And he seems to be right, based on the papers they've got up on the website.

[2] Or you could say that FIRE output is fixed (perhaps at 0), and all changes in nominal FIRE output represents price changes. Again, this problem can't be resolved empirically, nor does it go away simply because you adopt a utility-based view of value.

[3] Bob Fitch had some smart things to say about the need to distinguish productive and unproductive labor.

Sunday, April 10, 2011

The Financial Crisis and the Recession: Two Datapoints for the Skeptics

One of the most dramatic features of the financial crisis, for those who were following it obsessively in the autumn of 2008, was the near-freezing up of the commercial paper market. Commercial paper is short-term debt sold in markets rather than advanced by banks. It's mostly very short maturity -- days, weeks or months, not years. It's generally cheaper than other forms of financing, but firms that rely on it need to be able to borrow more or less continuously. Doubts about their financial condition, or even the suspicion that other lenders might have doubts, can quickly push them up against their survival constraint. This is what happened to a number of financial institutions -- most spectacularly Lehman Brothers -- in the third quarter of 2008. The breakdown in the commercial paper market was one of the things that convinced people the financial universe was imploding, and taking the real economy down with it.

The story, implicit or explicit, was that the suddenly reduced or uncertain value of financial assets, and the seizing-up of the interbank markets, left banks unable or unwilling to hold the liabilities of nonfinancial businesses, i.e., to lend. These businesses found themselves unable to finance new investment or even routine operations, leading to the Great Recession. This is essentially the same story that Milton Friedman told (and Peter Temin, among others, criticized), about the Great Depression, but it's also more or less the consensus view of the 2008-09 crisis among New Keynesian economists. For example:

The same story was widespread in the business journalism world, with people like Andrew Ross Sorkin writing, "Commercial paper, the workaday stuff that lets companies make payroll, was suddenly viewed as radioactive -- and business activity almost stopped in its tracks." Most importantly, this was the view of the crisis that motivated -- or at least justified -- the choice of both the Bush and Obama administrations to make strengthening bank balance sheets their number one priority in the crisis. But is it right? There are reasons for doubt.A large decrease in the value of asset holdings of financial institutions resulted in dramatic intensification of the agency problems in those institutions ... Credit spreads widened and credit rationing became widespread. The diminished ability to finance the acquisition of capital goods resulted in huge cutbacks of all types of investment.

|

| Data from FRED. |

The implication: The state of the interbank lending market isn't necessarily informative about the availability of credit to nonfinancial firms. It's perfectly possible that lots of big banks had made lots of stupid bets in the real estate market, and once this became known other banks were unwilling to lend to them. But they remained perfectly willing to lend to everyone else -- perhaps even on more favorable terms, since those funds had to go somewhere. The divergence in commercial paper rates is hardly dispositive, of course, but it at least suggests that the acute phase of the financial crisis was more of a problem for the financial sector specifically than for the economy as a whole

Second. Sorkin calls commercial paper "the workaday stuff that lets companies meet payroll." This kind of language was everywhere for a while -- that the financial crisis threatened to stop the flow of short-term credit from banks, and that without that even the most routine business functions would be impossible.

One of the central political-economic facts of our time is that public discussion of the economy is entirely dominated by finance. The interests of banks differ from those of other businesses on many dimensions; one of them is banks' dependence on short-term financing. Financial firms are defined by the combination of short-term liabilities and long-term assets; they need to borrow every day; that's why they're subject to runs. The fear of not being able to make payroll if you're cut off, even briefly, from financial markets, is perfectly reasonable, if you're a bank.

But if you're not?

In fact, short-term debt is large relative to cashflow only for financial firms. Nonfinancial firms don't finance operating expenses through debt, only investment. (And inventories and goods-in-progress, which are largely financed by credit from customers and suppliers, rather than from banks.) From Compustat:

Short-term debt as a fraction of total debt

| Sector | Median | Mean |

| FIRE | 0.56 | 0.55 |

| Non-FIRE | 0.16 | 0.23 |

Short-term debt as a fraction of cashflow

| Sector | Median | Mean |

| FIRE | 7.53 | 15.1 |

| Non-FIRE | 0.35 | 0.71 |

Short-term debt as a fraction of revenue

| Sector | Median | Mean |

| FIRE | 0.78 | 1.64 |

| Non-FIRE | 0.04 | 0.08 |

This isn't a secret; but it's striking how different are the financing structures of financial and nonfinancial firms, and how little that difference has penetrated into public debate or much of the economics profession. For the median financial firm, losing access to short-term finance would be equivalent to a 70 percent fall in revenues; few could survive. For the median nonfinancial firm, by contrast, loss of access to short-term finance would be equivalent to a fall in revenues of just 4 percent. Short-term finance is just not that important to nonfinancial firms.

So, the breakdown in short-term credit markets was largely limited to financial firms, and financial firms are anyway the only ones that really depend on short-term credit. I don't claim these two pieces of evidence are in any way definitive -- I've got a long paper on this question in the works, which, well, won't be definitive either -- but they are at least consistent with the story that the financial crisis, on the one hand, and the fall of employment and output, on the other, were more or less independent outcomes of the collapse of the housing bubble, and that the state of the banks was not the major problem for the real economy.

EDIT: For the life of me, I can't get either graphs or tables to look good in Blogger.

Saturday, April 9, 2011

Summers on Microfoundations

From The Economist's report on this weekend's Institute for New Economic Thinking conference at Bretton Woods:

And that's it it -- I promise! -- on microfoundations, methodology, et hoc genus omne in these parts, at least for a while. I have a couple new posts at least purporting to offer concrete analysis of the concrete situation, just about ready to go.

Pretty definitive, no?The highlight of the first evening's proceedings was a conversation between Harvard's Larry Summers, till recently President Obama's chief economic advisor, and Martin Wolf of the Financial Times. Much of the conversation centred on Mr Summers's assessments of how useful economic research had been in recent years. Paul Krugman famously said that much of recent macroeconomics had been "spectacularly useless at best, and positively harmful at worst". Mr Summers was more measured... But in its own way, his assessment of recent academic research in macroeconomics was pretty scathing.

For instance, he talked about all the research papers that he got sent while he was in Washington. He had a fairly clear categorisation for which ones were likely to be useful: read virtually all the ones that used the words leverage, liquidity, and deflation, he said, and virtually none that used the words optimising, choice-theoretic or neoclassical (presumably in the titles or abstracts). His broader point—reinforced by his mentions of the knowledge contained in the writings of Bagehot, Minsky, Kindleberger, and Eichengreen—was, I think, that while it would be wrong to say economics or economists had nothing useful to say about the crisis, much of what was the most useful was not necessarily the most recent, or even the most mainstream. Economists knew a great deal, he said, but they had also forgotten a great deal and been distracted by a lot.

Even more scathing, perhaps, was his comment that as a policymaker he had found essentially no use for the vast literature devoted to providing sound micro-foundations to macroeconomics.

And that's it it -- I promise! -- on microfoundations, methodology, et hoc genus omne in these parts, at least for a while. I have a couple new posts at least purporting to offer concrete analysis of the concrete situation, just about ready to go.

Tuesday, April 5, 2011

The Bond's Eye View of the Ivory Coast

I joked a while back that any statement in the business press that something is good or bad needs to be followed with an implicit "for bondholders." But it's not really a joke. Here's the Financial Times with the view from the bonds of the civil war in the Ivory Coast:

But there's a more serious point here, too. The only people in the rich world who have both an interest in what happens in the Ivory Coast, and the resources to act on it, are the owners of Ivoirian government bonds.

Of course this isn't strictly true. There might be foreign owners of private Ivoirian assets. But in fact there doesn't seem to be many: Of the country's $11 billion in external debt, $8.5 billion, according to the BIS, is public and all the remaining $2.5 billion private debt is publicly guaranteed. And of course there are firms and speculators in the cocoa industry, but they aren't going to as interested in the Ivory Coast specifically, and more importantly, they don't have the same access to the peak institutions of capitalism. It's the Financial Times, not the Commodities Times or even the International Trade Times. So it's perfectly natural for the FT to take the bond's eye view; to a first approximation, the bondholders are the representatives of the capitalist class as a whole with respect to the Ivory Coast.

[Laurent Gbagbo's] generals are negotiating a ceasefire at pixel time while the French think he’ll probably leave Ivory Coast within hours, after a heavy cost in bloodshed. But a brand new day for the Ivorian state?There it is: A new day for the Ivoirian state = resumption of debt payments.

If you’ve been watching the levitating prices on the country’s (defaulted) 2032 bond, you might think that. Having been rallying for some time, the bond is now priced more generously than before a $29m coupon payment failed in January... This is quite some faith in the ability — willingness — of Gbagbo’s successor, Alassane Ouattara, to resume debt service.

But there's a more serious point here, too. The only people in the rich world who have both an interest in what happens in the Ivory Coast, and the resources to act on it, are the owners of Ivoirian government bonds.

Of course this isn't strictly true. There might be foreign owners of private Ivoirian assets. But in fact there doesn't seem to be many: Of the country's $11 billion in external debt, $8.5 billion, according to the BIS, is public and all the remaining $2.5 billion private debt is publicly guaranteed. And of course there are firms and speculators in the cocoa industry, but they aren't going to as interested in the Ivory Coast specifically, and more importantly, they don't have the same access to the peak institutions of capitalism. It's the Financial Times, not the Commodities Times or even the International Trade Times. So it's perfectly natural for the FT to take the bond's eye view; to a first approximation, the bondholders are the representatives of the capitalist class as a whole with respect to the Ivory Coast.

Subscribe to:

Posts (Atom)