What happens to the economy as the dollar falls? ...Over time, Americans notice that British goods have become more expensive in comparison to domestically produced goods. In other words, the price of U.S.-made sweaters becomes cheaper relative to the price of sweaters imported from Britain. This will lead us to buy fewer sweaters from Britain and more domestically manufactured sweaters.

At the same time, the British notice that American goods have become relatively inexpensive in comparison to goods made at home. This means it takes fewer pounds to buy a sweater made in the United States, so the British will buy more sweaters made in the United States and fewer of their domestically manufactured sweaters.Indeed it's not. Changes in prices induce changes in transaction volumes that smoothly restore equilibrium, is the first article of the economist's catechism. But how much a given volume responds to a given price change, and whether the response is reliable and strong enough to make the resulting equilibrium relevant to real economies, are empirical questions. You could tell a similar parable about an increase in the minimum wage leading to a lower demand for low-wage labor, but as I'm sure

While American producers notice the increased demand for their exports, allowing them to raise their prices somewhat and still sell more than they had before the dollar fell. Similarly, for British exporters to continue selling they must lower prices.

Thus, as everyone eventually adjusts to the fall in the dollar, the trade deficit shrinks. This is not new economics by any stretch...

So what's the evidence on this point?

{kind=link}

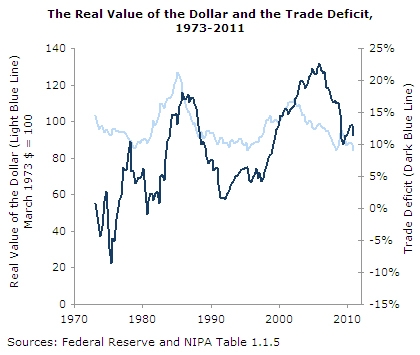

Still, isn't the picture is basically consistent with the story that when the dollar declines, US imports get more expensive and fall, and US exports get cheaper and rise? Not necessarily:

Click the graph to make it legible.

In a world where trade flows were mainly governed by exchange rates, a country's imports and exports would show a negative correlation. After all, the same exchange-rate change that makes exports more expensive on world markets makes imports cheaper here, and vice versa. But that isn't what we see at all. Except in the 1980s (when the exchange rate clearly did matter, but not in the way

(This discrepancy between real-world trade patterns and the textbook vision applies to almost all industrialized countries, and always has. It was noticed long ago by Robert Triffin, who brought it up to argue that movements in relative price levels did not govern trade patterns under the gold standard, as Ricardo and his successors had claimed. But it is just a strong counterargument to today's conventional wisdom that exchange rates govern trade.)

So if changes in exchange rates don't drive trade, what does? Lots of things, many of them no doubt hard to measure, or to influence through policy. But one obvious candidate is changes in incomes. One of the big advances of the first generation of Keynesian economists -- people like Triffin, and especially Joan Robinson -- was to show how, just as prices (the wage and interest rates) fail to equilibrate the domestic economy, leaving aggregate income to adjust, relative prices internationally don't equilibrate the global economy, leaving output or growth rates to adjust. In the short run, business cycle-type fluctuations reliably involve changes in investment and consumer-durable purchases larger disproportionate to the change in output as a whole; given the mix of traded and non-trade goods for most countries, this creates an allometry in which short-run changes in output are accompanied by even larger short-run changes in imports and exports. For a country that runs a trade deficit in "normal" times, this means that recessions are reliably associated with smaller deficits and booms with larger ones. In the long run, there is also a reliable tendency for increments to income to involve demand for a changing mix of goods, with a greater share of demand falling on "leading sectors," historically manufactured goods. (The flipside of this is Engels' law, which states that the share of income spent on food falls as income rises.) Given that both a country's mix of industries and its trade partners are relatively fixed, this creates a stable relationship between relative growth rates and trade balance movements. Neither of these channels is perfectly reliable, by any means -- and the whole point of the industrial policy is to circumvent the second one -- but they are still much stronger influences on trade flows than exchange rates (or other relative prices) are.

So with that in mind, let's look at another version of the graph. This one shows the year-over-year change in the trade balance as a share of GDP, the same change as predicted by an OLS regression on total GDP growth over the past three years, and as predicted by the change in the value of the dollar over the past three years. [1]

It will be legible if you click it.

It will be legible if you click it.Not surprisingly, neither prediction gives a terribly close fit. But qualitatively, at least, the predictions based on GDP do a reasonable job: They capture every major worsening and improvement in the trade balance. True, they under-predict the improvement in the trade balance in the later 80s -- the Plaza Accords mattered -- but it's clear that if you knew the rate of GDP growth over the next three years, you could make a reasonably reliable prediction about the the behavior of the trade balance. Knowing the change in the value of the dollar, on the other hand,wouldn't help you much at all. (And just to be clear, this isn't about the particular choice of three years. Two years and four years look roughly similar, and at a one-year horizon exchange rates aren't predictive at all.)

Here's another presentation of the same data, a scatterplot comparing the three-year change in the trade balance to the three-year growth of GDP (blue, left axis) and three-year change in the exchange rate (red, right axis). Again, while the correlation is fairly loose for both, it's clearly tighter for GDP. All the periods of strongest improvement in the trade balance are associated with weak GDP growth, and vice versa; similarly all the periods of strong GDP growth are associated with worsening of the trade balance, and vice versa. There's no such consistent association for the trade balance and changes in the exchange rate.

If you want to be able to read the graph, you should click it.

The fit could be improved by using some measure of disposable income -- ideally adjusted for wealth effects -- in place of GDP, and by using some better measure of relative prices in place of the exchange-rate index -- altho there's some controversy about what that better measure would be. And theoretically, instead of just the three-year change, you should use the individual lags.

Still, the takeaway, if you're a policymaker, is clear. If you want to improve the trade balance, slower growth is the way to go. And if you want to boost growth, you probably are going to have to ignore the trade balance. Personally, I want door number two. I assume

[1] Technicalities. I separately regressed the changes in imports and exports (as a percent of GDP) over three years earlier, on the percentage change over the same period in GDP and in the Fed's trade-weighted major-partners dollar index, respectively. It's all quarterly data, downloaded from FRED. The graphs shows the predicted values from the two regressions. This is admittedly crude, but I would argue that the more sophisticated approaches are in some respects less appropriate for the specific question being addressed here. For example, suppose hypothetically that a currency devaluation really did tend to improve the trade balance, but that it also tended to raise GDP growth, raising imports and offsetting the initial improvement. From an analytic standpoint, it might be appropriate to correct for the induced GDP change to get a better estimate of the pure exchange-rate effect. But from a policy perspective, the offsetting growth-imports effect has to be taken into account in evaluating the effects of a devaluation, just as much as the initial trade-balance improvement. Maybe we should say: Academics are interested in partial derivatives, policymakers in total derivatives?

EDIT: Oops! How did I not notice that this article was by somebody named David Rosnick, not Dean Baker? Makes me feel a bit better -- I know Dean does share this article's basic view of trade and the dollar, but I would hope his take would be a little less dependent on textbook syllogisms, and a little more attentive to actual patterns of trade. Clothing from the UK is hardly representative of US imports; to the extent we do import any, it's like to be high-end branded stuff that is particularly price-inelastic.

The Slack Wire: Do Prices Matter? >>>>> Download Now

ReplyDelete>>>>> Download Full

The Slack Wire: Do Prices Matter? >>>>> Download LINK

>>>>> Download Now

The Slack Wire: Do Prices Matter? >>>>> Download Full

>>>>> Download LINK L0