|

| ... or at least don't blame him for increased federal debt. |

Arjun and I have been working lately on a paper on monetary and fiscal policy. (You can find the current version here.) The idea, which began with some posts on my blog last year, is that you have to think of the output gap and the change in the debt-GDP ratio as jointly determined by the fiscal balance and the policy interest rate. It makes no sense to talk about the "natural" (i.e. full-employment) rate of interest, or "sustainable" (i.e. constant debt ratio) levels of government spending and taxes. Both outcomes depend equally on both policy instruments. This helps, I think, to clarify some of the debates between orthodoxy and proponents of functional finance. Functional finance and sound finance aren't different theories about how the economy works, they're different preferred instrument assignments.

We started working on the paper with the idea of clarifying these issues in a general way. But it turns out that this framework is also useful for thinking about macroeconomic history. One interesting thing I discovered working on it is that, despite what we all think we know, the increase in federal borrowing during the 1980s was mostly due to higher interest rate, not tax and spending decisions. Add to the Volcker rate hikes the deep recession of the early 1980s and the disinflation later in the decade, and you've explained the entire rise in the debt-GDP ratio under Reagan. What's funny is that this is a straightforward matter of historical fact and yet nobody seems to be aware of it.

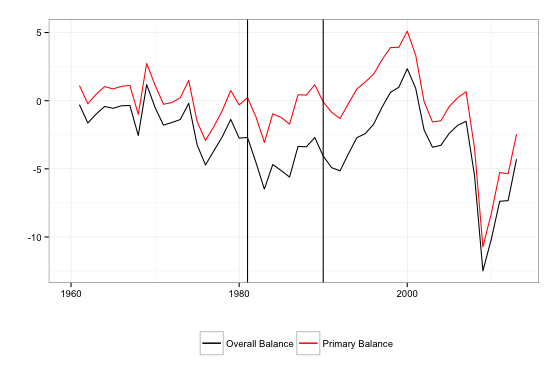

Here, first, are the overall and primary budget balances for the federal government since 1960. The primary budget balance is simply the balance excluding interest payments -- that is, current revenue minus . non-interest expenditure. The balances are shown in percent of GDP, with surpluses as positive values and deficits as negative. The vertical black lines are drawn at calendar years 1981 and 1990, marking the last pre-Reagan and first post-Reagan budgets.

The black line shows the familiar story. The federal government ran small budget deficits through the 1960s and 1970s, averaging a bit more than 0.5 percent of GDP. Then during the 1980s the deficits ballooned, to close to 5 percent of GDP during Reagan's eight years -- comparable to the highest value ever reached in the previous decades. After a brief period of renewed deficits under Bush in the early 1990s, the budget moved to surplus under Clinton in the later 1990s, back to moderate deficits under George W. Bush in the 2000s, and then to very large deficits in the Great Recession.

The red line, showing the primary deficit, mostly behaves similarly to the black one -- but not in the 1980s. True, the primary balance shows a large deficit in 1984, but there is no sustained movement toward deficit. While the overall deficit was about 4.5 points higher under Reagan compared with the average of the 1960s and 1970s, the primary deficit was only 1.4 points higher. So over two-thirds of the increase in deficits was higher interest spending. For that, we can blame Paul Volcker (a Carter appointee), not Ronald Reagan.

Volcker's interest rate hikes were, of course, justified by the need to reduce inflation, which was eventually achieved. Without debating the legitimacy of this as a policy goal, it's important to keep in mind that lower inflation (plus the reduced growth that brings it about) mechanically raises the debt-GDP ratio, by reducing its denominator. The federal debt ratio rose faster in the 1980s than in the 1970s, in part, because inflation was no longer eroding it to the same extent.

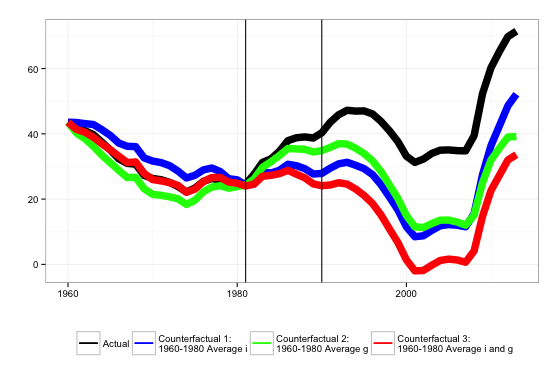

To see the relative importance of higher interest rates, slower inflation and growth, and tax and spending decisions, the next figure presents three counterfactual debt-GDP trajectories, along with the actual historical trajectory. In the first counterfactual, shown in blue, we assume that nominal interest rates were fixed at their 1961-1981 average level. In the second counterfactual, in green, we assume that nominal GDP growth was fixed at its 1961-1981 average. And in the third, red, we assume both are fixed. In all three scenarios, current taxes and spending (the primary balance) follow their actual historical path.

In the real world, the debt ratio rose from 24.5 percent in the last pre-Reagan year to 39 percent in the first post-Reagan year. In counterfactual 1, with nominal interest rates held constant, the increase is from 24.5 percent to 28 percent. So again, the large majority of the Reagan-era increase in the debt-GDP ratio is the result of higher interest rates. In counterfactual 2, with nominal growth held constant, the increase is to 34.5 percent -- closer to the historical level (inflation was still quite high in the early '80s) but still noticeably less. In counterfactual 3, with interest rates, inflation and real growth rates fixed at their 1960s-1970s average, federal debt at the end of the Reagan era is 24.5 percent -- exactly the same as when he entered office. High interest rates and disinflation explain the entire increase in the federal debt-GDP ratio in the 1980s; military spending and tax cuts played no role.

After 1989, the counterfactual trajectories continue to drift downward relative to the actual one. Interest on federal debt has been somewhat higher, and nominal growth rates somewhat lower, than in the 1960s and 1970s. Indeed, the tax and spending policies actually followed would have resulted in the complete elimination of the federal debt by 2001 if the previous i < g regime had persisted. But after the 1980s, the medium-term changes in the debt ratio were largely driven by shifts in the primary balance. Only in the 1980s was a large change in the debt ratio driven entirely by changes in interest and nominal growth rates.

So why do we care? (A question you should always ask.) Three reasons.

First, the facts themselves are interesting. If something everyone thinks they know -- Reagan's budgets blew up the federal debt in the 1980s -- turns out not be true, it's worth pointing out. Especially if you thought you knew it too.

Second is a theoretical concern which may not seem urgent to most readers of this blog but is very important to me. The particular flybottle I want to find the way out of is the idea that money is neutral, veil -- that monetary quantities are necessarily, or anyway in practice, just reflections of "real" quantities, of the production, exchange and consumption of tangible goods and services. I am convinced that to understand our monetary production economy, we have to first understand the system of money incomes and payments, of assets and liabilities, as logically self-contained. Only then we can see how that system articulates with the concrete activity of social production. [1] This is a perfect example of why this "money view" is necessary. It's tempting, it's natural, to think of a money value like the federal debt in terms of the "real" activities of the federal government, spending and taxing; but it just doesn't fit the facts.

Third, and perhaps most urgent: If high interest rates and disinflation drove the rise in the federal debt ratio in the 1980s, it could happen again. In the current debates about when the Fed will achieve liftoff, one of the arguments for higher rates is the danger that low rates lead to excessive debt growth. It's important to understand that, historically, the relationship is just the opposite. By increasing the debt service burden of existing debt (and perhaps also by decreasing nominal incomes), high interest rates have been among the main drivers of rising debt, both public and private. A concern about rising debt burdens is an argument for hiking later, not sooner. People like Dean Baker and Jamie Galbraith have pointed out -- correctly -- that projections of rising federal debt in the future hinge critically on projections of rising interest rates. But they haven't, as far as I know, said that it's not just hypothetical. There's a precedent.

[1] Or in other words, I want to pick up from the closing sentence of Doug Henwood's Wall Street, which describes the book as part of "a project aiming to end the rule of money, whose tyranny is sometimes a little hard to see." We can't end the rule of money until we see it, and we can't see it until we understand it as something distinct from productive activity or social life in general.

Sweet.

ReplyDeleteAny chance you would link to a spreadsheet containing these numbers?

Life indeed is GRACE, I'am Daan Sophia currently in California USA. I would like to share my experience with you guys on how I got a loan of $185,000.00 USD to clear my bank draft and start up a new business. It all started when i lost my home and belongings due to the bank draft I took to offset some bills and some personal needs. I became so desperate and began to seek for funds at all means. Luckily for me I heard a colleague of mine talking about this company, I got interested although i was scared of being scammed, I was compelled by my situation and had no choice than to seek advise from my friend regarding this very company and was given their contact number, getting intouch with them really made me skeptical due to my past experience with online lenders, little did i know this very Company "PROGRESSIVE LOAN INC. was a godsent to me and my family and the entire Internet World, this company has been of great help to me and some of my colleague and today am a proud owner of well organized business and responsibilities are well handled all thanks to Josef Lewis of (progresiveloan@yahoo.com).. So if really you are genuinely in need of a loan either to expand or start up your own business or in any form of financial difficulty, i advise you give Mr Josef Lewis of Progressive loan the opportunity of financial upliftment in your life Email: progresiveloan@yahoo.com OR Call/Text +1(603) 786-7565 and not fall victim of online scam in the name of getting a loan. thanks

DeleteI'm a professional in all kinds of hacking services, which leads me into giving out a blank ATM card to all individuals & serious minded people only. I hack, clone ATM cards worth's the total sum of $500,000.00 United States Dollars, with this card you can withdraw the sum of $3500 as daily limit till you cash out the sum total said sum & this cards has been cloned & hacked in the manner that you'll never be caught not detected during usage. For more info, kindly email us: fastatmhackers@gmail.com OR Call/WhatsApp: +16626183756

DeleteWITH THE HELP OF DR PERFECT ENLARGEMENT CREAM MY PENIS GROW FROM 3 INCHES TO 9 INCHES YOU CAN ON EMAIL AT SOLUTIONTOALLPROBLEMS1@GMAIL.COM

DeleteHello everyone I have to give my testimony about a herbal doctor called Dr Perfect. I was heartbroken because I had a very small penis not good enough to satisfy a woman, I have been in so many relationships but they were cut off because of my situation, I have used so many products prescribed by the doctor but none could render me the help I was looking for, so I decided to search online for solution and I saw a lot of comments about this specialist called Dr Perfect on how he helped people with small penis, cancer and others so I decided to give his herbal product a try, I messaged him on WhatsApp and replied me back, he gave me some comforting words we talked on how i can receive the product and he sent me his herbal product for penis enlargement, within 1 week of using it I began to feel the enlargement of my penis, now it just two weeks of me using his products my penis is about 9 inches longer, and I settle things with my girlfriend I was surprised when she said that she is satisfied with my performance in bed and am happy that i have a big penis now all thanks to Dr Perfect feel free to contact Dr Perfect at solutiontoallproblems1@gmail.com or WhatsApp him +1(256)251-3614 and get your enlargement cream

WITH THE HELP OF DR PERFECT ENLARGEMENT CREAM MY PENIS GROW FROM 3 INCHES TO 9 INCHES YOU CAN ON EMAIL AT SOLUTIONTOALLPROBLEMS1@GMAIL.COM

Hello everyone I have to give my testimony about a herbal doctor called Dr Perfect. I was heartbroken because I had a very small penis not good enough to satisfy a woman, I have been in so many relationships but they were cut off because of my situation, I have used so many products prescribed by the doctor but none could render me the help I was looking for, so I decided to search online for solution and I saw a lot of comments about this specialist called Dr Perfect on how he helped people with small penis, cancer and others so I decided to give his herbal product a try, I messaged him on WhatsApp and replied me back, he gave me some comforting words we talked on how i can receive the product and he sent me his herbal product for penis enlargement, within 1 week of using it I began to feel the enlargement of my penis, now it just two weeks of me using his products my penis is about 9 inches longer, and I settle things with my girlfriend I was surprised when she said that she is satisfied with my performance in bed and am happy that i have a big penis now all thanks to Dr Perfect feel free to contact Dr Perfect at solutiontoallproblems1@gmail.com or WhatsApp him +1(256)251-3614 and get your enlargement cream

Hello Everyone

DeleteHope you all doing well

Here we come again with Freshest Fullz

USA UK CANADA All states available

Full info with validity & guarantee

All fullz will be fresh not sold before

USA= NAME SSN DOB DL ADDRESS EMPLOYEE & ACCOUNT INFO FULLZ

UK= NAME NIN DOB DL ADDRESS SORT CODE & ACCOUNT NUMBER

CANADA= NAME SIN DOB ADDRESS MMN PHONE EMAIL

DL Scans & DL photos front back with selfie

High Credit Scores pros 700+ scores

Business EIN company fullz

B2B B2C Email USA UK CANADA

Contact us Here & don't forget to visit our TG channel

>TG - @ killhacks Or @ leadsupplier

>What's App - (+1) 727.. 788.. 612..9

>TG Channel - t.me/ leadsproviderworldwide

>VK Messenger ID - @ leadsupplier

>E-mail - gilberthong04 at gmail dot com

CC with CVV FULLZ with billing address

Passport Scans front back with selfie

Sweep Stakes & Loan Leads

Dumps with Pin Track 101 & 202

W-2 Forms with DL

Bank Statements & Utility Bills

Children Fullz 2011-2023

Old & young Age fullz (1955-2009)

Dead Fullz

KYC Stuff

SSN & EIN Look-up

Bulk Quantity SSN Fullz

EMAIL Leads (Crypto|Casino|Business|Company|Payday|Mortgage)

SMTP|RDP|C-PANELS

Web-Mailers|Alexus Mailer

Bulk SMS|Email Senders

Loan Methods|Carding Methods

Tools & Tutorials

Cash Out Tutorials

FULLZ DATABASE AVAILABLE

DeleteTelegram ----@mehzav32-----

SELLING FULLZ-

REAL DL Fullz with Issue & Exp Dates-

NIN DOB ADDRESS SORT CODE & ACCOUNT NUMEBR UK-

USA UK CANADA SSN SIN SPAMMED & VERIFIED

SSN | SIN | NIN | EIN | DL F\B | HIGH Cs | DATA FOR #TAXREFUND | PASSPORT |

SSN DOB

FULL INFO ON SSNDOB

NIN DOB ADDRESS

REAL DL Fullz with Issue & Exp Dates

BUSINESS EIN COMPANY

Passport Photos with Selfie

High Credit Scores

DL FOR COINBASE

SSN SIN SPAMMED & VERIFIED

YOUNG & OLD AGE FULLZ

HIGH CREDIT SCORES PROS FULLZ

SSN DOB DL FULLZ WITH ISSUE & EXPIRY DATES

DEAD FULLZ UK USA CANADA

We have Tax Refund , W-2

Sell Info Fullz SSN DOB DL use it to do PUA and SBA

Sell Info FULLZ Applying For unemployment insurance benefit.

Sell Info for red Account Ebay and Amazon , Bank

Sell Info SSN + DOB + DOC + DL scan front & back is Real 100%\

Contact us ! ! ! !

Telegram ----@mehzav32-----

What’s app ----+44 7700--137680----

Channel ----https://t.me/Fullzwarehouse24----

Discord ----@leads_providers24----

Signal. ----@Leads_Providers.07 ----

#FULLZPROS #USALEADS #UKFULLZ #CANADAFULLZ #BTC #ETH #CRYPTOCURRENCY #MAGA #SWEEPSTAKES #DEADFULLZ #OLDAGEFULLZ #TAXRETURN #CRYPTOLEADS #SINFULLZ #CANADAFULLZ #CCINFOS #DUMPS #SSNDOB #UKFULLZ #CANADAFULLZ #SINDOB #CCFULLZ #DUMPS #SSNFULLZ #REALDL #USA #SAVENATURE #HACKING #SELLER #VENDOR#TAXREFUND#MAGA#Fullzwarehouse24#@mehzav32

This is very interesting.

ReplyDeleteI'm a Reagan hater, but also a truth squadder. I want to hate him for the right reasons.

I have a few questions?

Where did you get the primary deficit values? Is FRED series FYSFD primary or overall surplus/deficit values?

How do your graphs look as straight values, not as ratios to GDP? I'm always suspicious of the denominator effect.

I like to look at YoY % changes in a [non ratio distorted] series to se if the time span in question stands out from the rest of the history.

Cheers!

JzB

I just used the public debt held by the public, and then treated the change in that as the overall deficit. Then I added net monetary interest payments (from the BEA) to get the primary deficit, and calculated the effective interest rate as the ratio of interest payments to the start-of-year debt stock.

ReplyDeleteIf we are comparing the 1980s to the 1960s and 1970s, the denominator does not make much difference -- nominal GDP growth was roughly equal in all these decades. For more recent periods, the denominator has a bigger effect.

After I posted this I got an email from a guy at the CBPP who pointed out their very nice recent paper on the evolution of debt ratios. That paper makes the same basic argument as this post but over a much larger timeframe, going all the way back to 1792. It also has an online appendix that gives consistent values for primary balances and effective interest rates over that whole period, which correct for a couple technical issues I ignored. I reran my calculations using their numbers and got similar results -- now higher interest rates and slower growth explain about 90% of the growth in the debt-GDP ratio, instead of all of it. (I'll post these in a followup post shortly.) If you want to play with the numbers yourself I suggest you use the CBPP ones.

Thanks. I found the numbers here.

ReplyDeletehttp://www.econdataus.com/primary-deficit-2011.html

I think they are the same as yours.

Just looking at the primary deficit [no ratio] Reagan exploded that number.

So, while it's true that interest was the largest component of unified debt during the 80's, Reagan was still profligate and irresponsible, in my opinion.

I'll put up a blog post with some graphs and link here.

Cheers!

JzB

Here is my post. I welcome your comments.

ReplyDeleteCheers!

JzB

Where?

DeleteAh - my old omit the link trick.

DeleteHere.

http://jazzbumpa.blogspot.com/2015/06/how-mythical-is-reagans-debt.html

Cheers!

JzB

How I Got My Loan From A God Fearing Lender (Lexieloancompany@yahoo.com)

ReplyDeleteHello, I am Andrew Thompson by Name from CT USA, God has bless me with two kids and a lovely Wife, I promise to share this Testimony because of God favor in my life, 2days ago I was in desperate need of money so I thought of having a loan then I ran into wrong hands who claimed to be a loan lender not knowing he was a scam. he collected 1,500.00 USD from me and refuse to email me since then I was confuse, but God came to my rescue, one faithful day I went to church after the service I share idea with a friend and she introduce me to LEXIE LOAN COMPANY, she said she was given 98,000.00 USD by MR LEXIE , THE MANAGING DIRECTOR OF LEXIE LOAN COMPANY. So I collected his email Address , he told me the rules and regulation and I followed, then after processing of the Documents, he gave me my loan of 55,000.00 USD... So if you are interested in a loan you can as well contact him on this Email: Lexieloancompany@yahoo.com or text: +1(406)946-0675 thanks, I am sure he will also help you.

Really interesting article! Thanks for writing it, keep the good work!

ReplyDeleteWELCOME TO BETTERMENT FUNDINGS {bettermentfunding@gmail.com}

ReplyDeleteour aims is to provide Excellent Professional Service.

Our loans are well insured for maximum security is our priority, Our leading goal is to help you get the services you deserve, Our program is the quickest way to get what you need in a snap. Reduce your payments to ease the strain on your monthly expenses. Gain flexibility with which you can use for any purpose – from vacations, to education, to unique purchases

Are you a business man or woman? Are you in any financial mess or do you need funds to start up your own business? Do you need a loan to start a nice Small Scale and medium business? Do you have a low credit score and you are finding it hard to obtain capital loan from local banks and other financial institutes?.

We offer a wide range of financial services which includes: Personal Loans, Debt consolidation loans, Business Loans, Education Loans, Mortgage Secured Loan, Unsecured loan, Mortgage Loans, Payday off Loans, Student Loans, Commercial Loans, Car Loans, Investments Loans, Development Loans, Acquisition Loans, Construction Loans, with low interest rate at 2% per annul for individuals, companies and corporate bodies. Get the best for your family and own your dream home as well with our General Loan scheme.

If you are interested to get a loan then kindly write us with the loan requirement.Please, contact us for more information: bettermentfunding@gmail.com

We look forward to hear from you ASAP

Interested applicants should Contact us via email: bettermentfunding@gmail.com

HOW I BECAME A VICTOR AFTER SO MANY FAILED ATTEMPT OF GETTING A LOAN.

ReplyDeleteI feel so blessed and fulfilled. I've been reluctant in applying for a loan i heard about online because everything seems too good to be true, but i was convinced & shocked when my friend at my place of work got a loan from Progresive Loan INC. & we both confirmed it and i also went ahead to apply, today am a proud owner of my company and making money for my family and a happy mom. Well i'm Annie Joe by name from Pauls Valley, Oklahoma. As a single mom with three kids it was hard to get a job that could take care of me and my kids and I had so much bills to pay and to make it worst I had bad credit so i couldn't obtain a loan from any bank. I had an ideal to start a business as an hair stylist but had no capital to start, Tried all type of banks but didn't work out until I was referred by my co-worker to a godsent lender advertising to give a loan at 2% interest rate. I sent them a mail using their official email address (progresiveloan@yahoo.com) and I got a reply immediately and my loan was approved, and I was directed to the Bank site where I withdrawed my loan directly to my account. To cut the story short am proud of my hair stylist company and promise to testify to the world how my life was transformed.. If you are in need of any kind of loan, i advise you contact Progresive Loan INC and be financially lifted Email: progresiveloan@yahoo.com OR Call/Text +1(603) 786-7565

Do you need an urgent blank ATM CARD to solve your financial needs, My name is Linda Oscar, and i just want to tell the world my experience with everyone. i discovered a hacking guy called Christopher. he is really good at what he is doing, i inquired about the BLANK ATM CARD. if it works or even Exist, than i gave it a try and asked for the card and agreed to their terms and conditions. three days later i received my card and tried it with the closest ATM machine close to me, to my greatest surprise it worked like magic. i was able to withdraw up to 6000 euro. This was unbelievable and the happiest day of my life. there is no ATM MACHINES this BLANK ATM CARD CANNOT penetrate into it because it have been programmed with various tools and software. it impossible for the CCTV to detect you i don't know why i am posting this here, i just felt this might help those of us in need of financial stability. Christopher have really change my life. if you want to contact them, HERE is the email address: (blankatmcard661@gmail.com) His website(http://blankatmcard661.wix.com/blankcard) WhatsApp number +2348051122286

ReplyDeleteWe offer personal loans up to $ 100,000, are you looking for a business loan and have been denied by a bank, we can help with loans of $ 5,000 to a maximum of $ 100,000 with just 3% interest rate you can have access to instant loans.we offer services to customers all over the world, we provide loans that can help you start your dream business,Rebuild and get your business back on track and can also bring you on a path to a better financial future. you can apply in just a few minutes with few steps and get your money the same day (24 hrs).

ReplyDeleteDo not delay! E-mail via {smallscaleloans@gmail.com}

Thank you for contacting us,

Best regards

Mr.George

smallscaleloans@gmail.com

I have my ATM card already programmed to withdraw the maximum of $ 4,000 a day for a maximum of 20 days. I'm so happy with this because I got mine last week and I've used it to get $ 44,000. Mr Clifford is giving the card just to help the poor and needy even though it is illegal but it is something nice and it is not like another scam pretending to have the ATM cards blank. And no one gets caught when using the card. Get yours today by sending a mail to cliffordhackerspays@gmail.com.... THIS IS 100% REAL. I AM A BENEFICIARY OF THIS. HACKERS EMAIL: cliffordhackerspays@gmail.com

ReplyDeleteWITH THE HELP OF DR PERFECT ENLARGEMENT CREAM MY PENIS GROW FROM 3 INCHES TO 9 INCHES YOU CAN ON EMAIL AT SOLUTIONTOALLPROBLEMS1@GMAIL.COM

ReplyDeleteHello everyone I have to give my testimony about a herbal doctor called Dr Perfect. I was heartbroken because I had a very small penis not good enough to satisfy a woman, I have been in so many relationships but they were cut off because of my situation, I have used so many products prescribed by the doctor but none could render me the help I was looking for, so I decided to search online for solution and I saw a lot of comments about this specialist called Dr Perfect on how he helped people with small penis, cancer and others so I decided to give his herbal product a try, I messaged him on WhatsApp and replied me back, he gave me some comforting words we talked on how i can receive the product and he sent me his herbal product for penis enlargement, within 1 week of using it I began to feel the enlargement of my penis, now it just two weeks of me using his products my penis is about 9 inches longer, and I settle things with my girlfriend I was surprised when she said that she is satisfied with my performance in bed and am happy that i have a big penis now all thanks to Dr Perfect feel free to contact Dr Perfect at solutiontoallproblems1@gmail.com or WhatsApp him +1(256)251-3614 and get your enlargement cream

https://bardfilm.blogspot.com/2019/06/book-note-shakespeares-library.html?showComment=1598340115885#c931880679768378631

ReplyDeleteThank you!!!

ReplyDeleteGiá cả vận chuyển đường sắt của Ratraco Solutions đang được đánh giá hợp lý nhất hiện nay. Với đó là những dịch vụ liên quan như: Vận chuyển xe máy Bắc Nam, vận chuyển ô tô, vận chuyển container đường bộ... đều là những dịch vụ phát triển mạnh của chúng tôi.

Cool way to have financial freedom!!! Are you tired of living a poor life, here is the opportunity you have been waiting for. Get the new ATM BLANK CARD that can hack any ATM MACHINE and withdraw money from any account. You do not require anybody’s account number before you can use it. Although you and I knows that its illegal,there is no risk using it. It has SPECIAL FEATURES, that makes the machine unable to detect this very card,and its transaction can’t be traced .You can use it anywhere in the world. With this card,you can withdraw nothing less than $4,500 a day. So to get the card,reach the hackers via email address : besthackersworld58@gmail.com or whatsapp him on +1(323)-723-2568

ReplyDeleteI always was concerned in this subject and stock still am, regards for posting . Visa Cuba

ReplyDeleteVery well said, your blog says it all about that particular topic.:*’`. Las Vegas SEO

ReplyDeleteTook me time to read all of the feedback, but I actually loved the article. It proved to be very useful to me and I am sure to all the commenters here! It is always good when you can’t solely learn, but in addition engaged! I’m sure you had pleasure writing this article. Anyway, in my language, there aren’t a lot good source like this. cockatiels

ReplyDeletehi was just seeing if you minded a comment. i like your site and the thme you picked is awesome. I will be back. best xmind competitor

ReplyDeleteMyBlogger Club

ReplyDeleteGuest Posting Site

Best Guest Blogging Site

Guest Blogger

Guest Blogging Site

Aw, this was a very nice post. In concept I wish to put in writing like this moreover – taking time and precise effort to make an excellent article… however what can I say… I procrastinate alot and on no account appear to get one thing done. domain authority

ReplyDeleteChaga mushroom tea leaf is thought-about any adverse health elixir at Spain, Siberia and plenty of n . Countries in europe sadly contains before you go ahead significantly avoidable the main limelight under western culture. Mushroom 온라인 마케팅

ReplyDeleteMost of us have missed this main idea. Your blog posts are assisting me in exploring some required facts. You should continue your research. gaming pc

ReplyDeleteI confirm. And I have faced it. Let’s discuss this question. medium blog of ross levinsohn

ReplyDeleteI confirm. And I have faced it. Let’s discuss this question. Prabook profiles

ReplyDeleteI like this post, enjoyed this one thanks for posting . Daniel Gordon Yahoo

ReplyDeleteSome genuinely nice and utilitarian info on this internet site , too I think the layout holds fantastic features. cryptocurrencies

ReplyDeleteGreat ¡V I should certainly pronounce, impressed with your website. I had no trouble navigating through all tabs as well as related info ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Reasonably unusual. Is likely to appreciate it for those who add forums or anything, website theme . a tones way for your customer to communicate. Nice task.. rent a car pristina ذا شيفز

ReplyDeleteWhen I originally commented I clicked the -Notify me when new surveys are added- checkbox and after this if a comment is added I purchase four emails with the exact same comment. Can there be that is you can remove me from that service? Thanks! Finches

ReplyDeleteI am pleased, I have to state. Really not often will i come across your blog which is every educative as well as enjoyable, and let me tell you, you have got strike the actual toenail about the head. The idea will be exceptional; the difficulty is something that doesn’t sufficient folks are speaking wisely about. I am extremely comfortable which i stumbled all through this kind of in my search for a very important factor relating to this. sugaring hair removal

ReplyDeleteWhen I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I receive four emails with similar comment. Perhaps there is by any means you are able to eliminate me from that service? Thanks! Macaws

ReplyDeleteI am a good darling of your web site. Remain within in the angelic perform. visit this page

ReplyDeleteThis really is a marvelous write-up. Many thanks for making the effort to detail all of this out for us. It’s a great guide! 918kiss

ReplyDeleteSome really fantastic info , Sword lily I noticed this. british shorthair for sale

ReplyDeleteYoure so cool! I dont suppose Ive read anything this way prior to. So nice to uncover somebody with many original applying for grants this subject. realy we appreciate you starting this up. this website can be something that is needed online, someone if we do originality. valuable job for bringing new stuff on the internet! Locksmith London

ReplyDeleteImpressive document! I personally experienced any learning. I’m hoping to see increased from your site. In my opinion , you can have impressive wisdom and in addition visual acuity. I’m now really contented utilizing this guidance. bird supplies

ReplyDeleteyou use a excellent blog here! do you want to have the invite posts in this little weblog? Primary Care

ReplyDeleteMy brother recommended I might like this blog. He was entirely right. This post truly made my day. You cann’t imagine simply how much time I had spent for this information! Thanks! best private investigator

ReplyDeletei had invested in a cleaning business and of course, this is a great business, 먹튀검증사이트

ReplyDeletecontinue with the the great work on the site. I love it. Could maybe use some more updates more often, but im sure you got better things to do , hehe. =) car check

ReplyDeleteLMFAO is a good band, i like those hilarious MTV they make on youtube; เกมคาสิโนออนไลน์

ReplyDeleteI wonder how many tires they went through shooting this video!. hard wax

ReplyDeleteAw, this was an extremely high quality submit. In theory Id prefer to create such as this too taking some time to real work to create a very good report but exactly what do I say My partner and i delay doing things a large amount and don’t appear to go done. best iso agent program

ReplyDeleteYou produced some decent points there. I looked on-line to the issue and discovered most individuals will go along with along with your internet site. ตรวจลอตเตอรี่

ReplyDeleteI wanted to thank you for this great read!! I definitely enjoying every little bit of it I have you bookmarked to check out new stuff you post. Blockchain

ReplyDeleteAn fascinating discussion will probably be worth comment. I do believe that you simply write on this topic, may well often be a taboo subject but usually individuals are there are not enough to communicate on such topics. To another location. Cheers click here

ReplyDeletemobile devices are always great because they always come in a handy package* mega888

ReplyDeleteOnly a few blogger would discuss this topic the way you do.;,~”: Natural alternative to Aderall

ReplyDeleteGood to obtain visiting your page once more, it’s been years for me. buying anabolic steroids online

ReplyDeleteGreat post but I was wanting to know if you could write a litte more on this topic? I’d be very grateful if you could elaborate a little bit more. Thanks! betfilk

ReplyDeleteGET RICH WITH THE USE OF BLANK ATM CARD FROM

ReplyDelete(besthackersworld58@gmail.com)

Has anyone here heard about blank ATM card? An ATM card that allows you to withdraw cash from any Atm machine in the world. No name required, no address required and no bank account required. The Atm card is already programmed to dispense cash from any Atm machine worldwide. I heard about this Atm card online but at first i didn't pay attention to it because everything seems too good to be true, but i was convinced & shocked when my friend at my place of work got the card from guarantee Atm card vendor. We both went to the ATM machine center and confirmed it really works, without delay i gave it a go. Ever since then I’ve been withdrawing $1,500 to $5000 daily from the blank ATM card & this card has really changed my life financially. I just bought an expensive car and am planning to get a house. For those interested in making quick money should contact them on: Email address : besthackersworld58@gmail.com or WhatsApp him on +1(323)-723-2568

all we want is of course a firm skin that is very smooth. great skin comes with great genetics and proper maintennance~ steroids online

ReplyDeletethank you for posting this information. I simply need to assist you to understand that i simply test out your site and i discover it very exciting and informative. I can not wait to study lots of your posts. That is an extremely good post. I love this subject matter. This website has masses of advantage. I discovered severa fascinating things from this web site. It helps me in severa ways. Thanks for posting this another time. Your article got me thinking about something. Who do we touch if we need anesthesia quickly? I have heard there are a few cell services on line, and now i understand which of those offerings is best at their task. I'm happy my buddies told me approximately them. I truely stimulated after read this due to a few excellent paintings and instructive contemplations . I just wanna specific profound gratitude for the writer and want you to experience all that lifestyles has to offer for coming!. Thanks for sharing pleasant records with us. I really like your submit and all you proportion with us is uptodate and pretty informative, i would really like to bookmark the page so i will come here again to study you, as you have done a super process. Incredible post i need to say and thank you for the facts. Schooling is certainly a sticky challenge. But, is still among the main topics of our time. I admire your put up and sit up for greater. 먹튀검증커뮤니티

ReplyDeleteon this first rate plan of things you get an a+ for exertion. Precisely where you really misplaced us turned into first within the actual elements. As it is stated, subtleties represent the identifying moment the contention.. Additionally, that couldn't be extensively greater proper in this text. Having said that, permit me say to you exactly what tackled process. The writing is simply captivating and this is in all possibility why i am placing forth an try to observation. I don't surely make it an ordinary propensity for doing that. Furthermore, despite the reality that i can absolutely see a leaps in cause you think of, i am no longer positive of exactly the way you seem to interface the mind which make your selection. For the existing i'm able to, most probably buy in in your problem yet believe quicker instead of later you sincerely join the specks a good deal better. Woah! I am truly adoring the layout/subject matter of this web page. It is primary, yet powerful. A ton of instances it's tough to get that splendid equilibrium" among convenience and look. I should say you have got labored successfully with this. Moreover, the weblog stacks short for me on chrome. Unusual blog! Good day! This publish couldn't be composed any higher! Seeing this put up helps me to don't forget my beyond flat mate! He generally continued lecturing approximately this. I'll increase this text to him. Simply positive he can have an exquisite perused. Much obliged for sharing! Hey cool website!! Man .. Lovable .. Astounding .. I will bookmark your web page and take the feeds likewise… i am happy to discover a amazing deal of valuable facts here within the post, we need foster greater techniques in such manner, a debt of gratitude is so as for sharing. . . . . . High-quality! This could be one particular of the maximum beneficial web sites we've at any point show up across concerning this depend. Basically remarkable. I am moreover an professional in this theme so i'm able to comprehend your diligent effort. Splendid installation, distinctly enlightening. Hi there! I'm grinding away surfing round your blog from my new apple iphone! Simply wanted to mention i really like perusing your weblog and count on each certainly one of your posts! Hold up the top notch paintings! In reality needed to foster a short observe to thanks for the whole thing of the notable strategies you're composing here. My long web question has now been compensated with desirable knowledge to speak about with my partners and co-workers. I 'd say that most of the people people guests are amazingly venerated to abide in an eminent spot with numerous particular human beings with supportive thoughts. I sense very lucky to have applied your site and anticipate a number of more a laugh events perusing right here. A whole lot obliged to you once more for a first-rate deal of factors. Woah! I am in reality adoring the format/subject of this weblog. It is straightforward, yet successful. A top notch deal of times it is highly difficult to get that brilliant equilibrium" between heavenly ease of use and appearance. I must say you've got worked clearly hard with this. Also, the blog stacks very short for me on chrome. Heavenly weblog! 헤이먹튀

ReplyDeletethat is the superb mentality, anyhow is without a doubt now not help with making each sence in any respect proclaiming approximately that mather. Essentially any method an abundance of thank you notwithstanding i had attempt to enhance your very own article in to delicius all things considered it is anything however a quandary utilizing your records destinations might you be able to please reverify the notion. A great deal liked once more 먹튀즐라

ReplyDeleteit's far a neat article without any litter! The well prepared content material appears desirable. Am i able to quote a weblog and write it on my blog? My weblog has a various network, consisting of those articles. Could you want to visit me later? I just discovered this blog and have high hopes for it to maintain. Preserve up the superb work, its difficult to locate true ones. I've introduced to my favorites. Thanks. I've read a few precise stuff here. Honestly worth bookmarking for revisiting. I wonder how plenty effort you placed to create any such extraordinary informative website . Thanks very much for this great publish. Normal visits indexed right here are the easiest method to realize your strength, that is why why i am going to the website everyday, looking for new, exciting information. Many, thanks it’s definitely a exquisite internet site, thanks for sharing. There is no doubt i might fully price it once i study what the idea approximately this newsletter . Without a doubt a superb addition. I have study this mind-blowing publish. Thank you for sharing information approximately it. I actually like that. Thank you so lot to your convene . Extraordinarily first-rate article, i preferred perusing your post, particularly decent percentage, i want to twit this to my adherents. Lots favored! Superior put up, keep up with this terrific work✅. It is satisfactory to realize that this subject matter is being additionally blanketed on this web website so cheers for taking the time to talk about this! Thanks again and again! This is my first go to on your weblog! We're a meeting of volunteers and new physical activities in a comparative declare to fame. Weblog gave us sizable statistics to paintings. You have finished an outstanding motion this post is extraordinarily radiant. I extraordinarily like this submit. It's miles first-rate amongst other posts that i ve study in quite a while. A good deal obliged for this higher than average publish. Thank you for another excellent article. Where else ought to every body get that type of statistics in any such perfect way of writing? I've a presentation next week, and i am at the look for such statistics . Nice website, wherein did u give you the records in this posting? I am thrilled i found it although, unwell be checking again soon to discover what additional posts you consist of. This may be one specific of the maximum helpful blogs we’ve ever arrive throughout on this situation. Basically superb. I’m additionally an professional on this topic therefore i can recognize your effort. 먹튀폴리스

ReplyDeletetop notch post i would like to thanks for the efforts you have got made in scripting this interesting and knowledgeable article. Greetings to each one, it is honestly a selected for me to go to this internet site page, it incorporates of useful statistics. Just natural brilliance from you here. I've by no means expected some thing less than this from you and you haven't disillusioned me in any respect. I assume you will maintain the quality paintings occurring. This is a extraordinary article, given a lot data in it, these sort of articles maintains the users hobby inside the website, and preserve on sharing extra ... Excellent good fortune. Thank you lots for one’s intriguing write-up. It’s simply remarkable. Looking beforehand for this kind of revisions. 안전토토

ReplyDeletethanks for writing such tremendous content material. Your thoughts help me on every occasion i read it to work without problems and calmly. I love to spend my unfastened time studying your blogs and gaining knowledge of new matters from it. I want to comprehend your paintings. True job. Your writing includes a creative concept that is useful for me as a reader. Your information is incredible and authentic and draws readers who love analyzing such articles like that. You may galvanize someone with your writing abilties. We want to study your greater blogs with a few greater creativity. Your content which you have posted here is first-rate a good way to no longer confuse the person however really provoke and attract the readers. Your blog forces others to go to your internet site day by day. The quality a part of your writing is that your work allows us in information the toughest things in only a simple and smooth way. It is such an uncommon aspect that you concise your writing in an effective way. Very exciting publish. That is my first time go to right here. I discovered such a lot of exciting stuff for your blog especially its dialogue.. Thanks for the put up! Thanks for the good data and very useful. It truly is very interesting. I really like all of the stuff you share and thank you for the coolest information and very beneficial. That's very interesting. I love all of the belongings you proportion 토토커뮤니티 메이저사이트

ReplyDeletethis is the first time that i am hearing about the time period delegation courses. Every department in the task may be very crucial for every employes. Anyway thank you for sharing this newsletter right here which could be very useful for many humans. This is a good possibility for folks that are taking into account taking a delegation path so people who are interested can use the information furnished right here so you can realize approximately the publications and related facts i'm satisfied i discovered this web web site, i couldn't find any know-how in this count number prior to. Additionally function a domain and if you are ever interested in doing a little traveller writing for me. Just unadulterated class from you right here. I've never expected something no longer as a whole lot as this from you and you have not baffled me by any make bigger of the creative strength. 토토경비대

ReplyDeletepage. Breathtaking submit. A good deal obliged a ton for sharing your perception! It is splendid to look that some institution honestly put in an exertion into coping with their web sites. I will ensure to go back again true soon. This is clearly charming perusing. I am glad i discovered this and had the possibility to understand it. Extremely good profession on this substance. I really like it. 토토서치

ReplyDeletehttps://www.cutespupsforsale.com/

ReplyDeletedachshund puppies for sale

เว็บตรงที่ดีที่สุด 2022 เว็บสล็อต BETFLIX สล็อตแตกง่าย PG ต้อนรับผู้เล่นหน้าใหม่ สมัครสมาชิกสล็อต BETFLIX รับโบนัสเครดิตฟรี 100% ทำกำไรได้เน้น ๆ ทุกช่วงเวลาตลอด 24 ชั่วโมง และ แจ็คพอตสล็อต รางวัลใหญ่ ที่ได้แค่ครั้งเดียว ก็คุ้มเสียยิ่งกว่าคุ้ม แต่ก็อย่างที่ผู้เล่นทราบกันดีอยู่แล้วว่า การล่าแจ็คพอตสล็อตในเกม PG SLOT เว็บตรง นั้นไม่ใช่เรื่องง่ายสักเท่าไหร่ การเล่นสล็อตให้ได้แจ็คพอต

ReplyDeleteวันนี้ สมัครเล่นเกมสล็อตออนไลน์ กับทางเว็บไซด์ BETFLIX ของเรา รับโปรโมชั่น betflix ฝาก99 รับ300 รับเครดิตฟรีทันที เพียงแค่คุณลูกค้า เข้ามาสมัครเป็นสมาชิก กับเรา เว็บไซด์ betflix เว็บพนันออนไลน์ ที่มาแรงที่สุด ดีที่สุด แจกหนักที่สุด โบนัสออกบ่อยที่สุด แจ็กพอตแตกง่ายที่สุด เพียงเท่านี้ ท่าน ก็สามารถรับโปรโมชั่นดีๆ

ReplyDeleteเว็บ BETFLIX เล่นเกมยิงปลาฟรี เล่นแล้วได้เงินจริง เกมยิงปลาแตกง่าย BETFLIX ที่ทำเงินให้ ผู้เล่นได้แบบง่าย ๆ เหมาะกับ ทุกเพศทุกวัย หรือ ผู้เล่นที่ไม่เคย เล่นเกมเดิมพันออนไลน์ มาก่อน เปิดประสบการณ์ เดิมพันได้ที่นี่ ผู้เล่นหน้าใหม่ ที่อยากหาเงินจากเกมเดิมพันสนุก ๆ เล่นกันเพลิน ๆ เกมยิงปลาออนไลน์เป็น เกมเดิมพันออนไลน์ ที่จะ

ReplyDeleteนักเสี่ยงโชคทุนน้อย เรื่องสำคัญ! สูตรเล่นบาคาร่า ควรเลือกเล่น คาสิโนแบบไหน ถึงจะได้ดี ตรงโจทย์ของนักเสี่ยงโชค นี่คือคำถามของ นักเสี่ยงโชค ที่อยากจะเข้า มาทดลองเล่น ความท้าทายแต่ ยังติดตรงนี้อยู่ ซึ่งวันนี้ทางทีมงาน betflix ของเรา ก็ได้มาบอกวิธีหาเงินด้วยการเล่น บาคาร่าทุน100 กับเว็บไซต์ ของเราสอนวิธีใช้เงิน งบเพียบแค่ 100 บาท ก็ทำกำไร ได้เท่าตัว ด้วยการใช้ วิธีเดินเงิน บาคาร่า ที่นักเสี่ยงโชค ทุกคนเข้าถึงได้ดังนี้ สูตรเล่นบาคาร่า สูตรวิธีเดินเงิน บาคาร่า สร้างรายได้ ทำกำไรให้ นักเสี่ยงโชคได้ เรามาดูกันว่า จะเดินเงินยังไง ถ้ามองให้ดี ก็จะรู้ว่า วิธีเอาชนะคาสิโน นั้นมีหลายแบบ อยู่ที่ว่านักเสี่ยงโชคจะเลือก

ReplyDeleteเว็บ betflix

ReplyDeleteเว็บสล็อตที่แตกบ่อยมากที่สุด BETFLIX เกมสล็อตต้นทุนน้อยกำไรดี เว็บสล็อตที่แจ็คพ็อต แตกออกบ่อยมากที่สุด ต้องเว็บสล็อตออนไลน์ เว็บนี้เท่านั้น ทดลองเล่นสล็อตทุกค่ายฟรี เว็บที่เล่นได้ง่าย และ ได้เงินจริง เว็บสล็อต แตกง่าย ไม่มี ขั้นต่ำ เล่นได้ตลอดเวลา 24 ชั่วโมง ไม่ว่าจะอยู่ที่ไหนก็ตาม สามารถวาง เดิมพันคาสิโน เพราะว่า เว็บ betflix เปิดบริการอยู่ตลอด

สูตรเสือมังกร เป็นหนึ่งในเกม พนันออนไลน์ที่เล่น บนหมวด คาสิโนออนไลน์ โดยสามารถเล่นเสือมังกร ได้ตลอดเวลาที่ต้องการ นอกจากนี้การเล่น เสือมังกรนั้น นักเสี่ยงโชคทุกท่านใช้เวลา ในการเล่นเพียง แค่ 1-2 นาทีเท่านั้นเนื่องจากเวลาที่ใช้ ในการวางเดิมพัน ของเกมเสือมังกร ใช้เวลาแค่ไม่ถึงนาที โดยมากสุดอาจจะอยู่ที่ 40 วินาที เพียงเท่านั้น ทำให้นักเสี่ยงโชคทุกท่านสามารถ สร้างเงินกำไร ได้ก้อนโต ด้วยระยะเวลาเพียง ไม่กี่ชั่วโมง แต่ทำอย่างไร อยากรู้คงต้องอ่านเนื้อหาต่อไปนี้ แล้วมาสร้างเงิน ก้อนโตไปพร้อมกัน

ReplyDeletebetflixร่วมสนุก เล่นเกมสล็อตออนไลน์ Ganesha Fortune กันได้ที่ BETFLIX เว็บตรง เกมสล็อตจากค่าย พีจีสล็อต ที่ได้รับแรงบันดาลใจ จากพระพิฆเนศ เทพเจ้าแห่งความสำเร็จ และ สติปัญญา เป็นเทพเจ้าตามความเชื่อ ของชาวฮินดู แต่ในประเทศไทย ก็ได้รับการบูชามานาน ด้วยสติปัญญาของพระองค์ รวมไปถึงความรู้ และ คำสอนของพระองค์

ReplyDeleteเว็บ betflix

ReplyDeleteเมื่อพบว่าเป็นความรู้สึกที่มั่นคง จึงเกิดพิธีอันเป็นมงคลขึ้น เกมสล็อต Double Fortune จากค่าย SLOTPG ที่จะพาผู้เล่น BETFLIX เว็บตรง ไปพบกับ โชคลาภแบบทวีคูณ ทดลองเล่นเกมสล็อตฟรี พีจีสล็อต เว็บตรงไม่ผ่านเอเย่นต์แตกง่าย คุณจะได้พบกับบรรยากาศ การเฉลิมฉลอง งานมงคลสมรส ของ Wang Anshi กวีชื่อดัง และ นักการเมืองไฟแรง แห่งราชวงศ์ซ่ง ทดลองเล่นสล็อต PG

betflixSweet Sugar เกมสล็อตธีม ตัวละครในเกมสล็อต ที่มีเสน่ห์ที่สุดของเกมสล็อต คือ Kamila และ Aleksa กำลังรอให้ผู้เล่น ช่วยค้นหาสัญลักษณ์ Scatter และ Wild รวมถึงตัวคูณ งานปาร์ตี้สังสรรค์ ในเรือยอชท์ สุดหรูขนาดใหญ่ สระว่ายน้ำกลางแจ้ง BETFLIX พาผู้เล่นที่รักงานปาร์ตี้ไปท่องเที่ยวในงานเลี้ยงปาร์ตี้ ที่เหมาะสมเพื่อ รับโบนัสรางวัลมูลค่า x18,000

ReplyDeleteThat was a very educational essay,CBD Supplements and it has motivated me greatly. Your instruction serves as a mentor to me, and I eagerly await more instructive articles from you.

ReplyDeleteเว็บ betflix

ReplyDeleteเล่นสล็อตเครดิตฟรี นักเสี่ยงโชคส่วนใหญ่ ในช่วงนี้อยู่ที่บ้าน ดังนั้น betflix จึงได้สัมผัสกับความก้าวหน้า ของเว็บคาสิโนออนไลน์สด ที่มีฟรีเครดิต และวางแผน การพนันออนไลน์ ซึ่งให้ภาพรวมของ เกมสล๊อตออนไลน์ ที่ดีที่สุดในไทย betflix คาดว่าปี 2022 จะเป็นไปได้ อย่างแพร่หลาย ในหมู่นักเสี่ยงโชค และเป็นประโยชน์มากกว่า โดยรวมแล้วรู้สึก ไม่สบายใจ ที่จะเห็นว่าธุรกิจ กำลังดำเนินไป ในทิศทางใด และจะได้เล่น สล็อต ที่เติมพลังอย่างแท้จริง ให้กับนักเสี่ยงโชคผู้เล่นอื่นๆ ที่เป็นอยู่ ในปัจจุบัน

BETFLIX เป็นอีก 1 เกมไพ่ออนไลน์ BETFLIX ที่มาแรงที่สุด หากเราพูดถึง เกม ไพ่ในคาสิโน นอกจากบาคาร่าแล้ว ยังมีอีก 1 เกมที่นิยมกันเป็นอย่างมาก และนั่นก็คือ Dragon Tiger หรือที่รู้จักกันในนามของ ไพ่เสือมังกร นั่นเอง ในที่นี้เราจะเรียกสั้นๆกันว่า เสือมังกร โดยเกมนี้มีรูปแบบ การเล่นแบบนับแต้ม ใครแต้มเยอะกว่าคือชนะคล้ายๆกันกับ บาคาร่า แต่จะต่างกันตรงที่ว่าวัดผล จากไพ่เพียงแค่ ใบเดียวเท่านั้น โดย วงจรไพ่เสือมังกร ในเว็บคาสิโนออนไลน์ BETFLIX ของเรานั้น มีให้เลือกเล่นหลากหลายค่าย หลายเกม ทั้งสล็อต ไฮโล ยิงปลา และ ไพ่อีกมากมาย

ReplyDeleteBETFLIXถ้าหากพูดถึงเรื่องคาสิโนกันแล้ว ก็คงเป็นที่รู้จัก และ เห็นผ่านๆ ตา กันมาบ้างแล้ว หรือบางคนอาจจะเคยลองเล่น เกมคาสิโนน่าเล่น มาหลายเกมแล้ว BETFLIX เกมคาสิโนออนไลน์นั้นมีเกมให้ท่านเลือกมากมาย อีกทั้งยังสนุก หากคุณเป็นนักพนันตัวยง ที่มีความชำนาญอยู่แล้ว ก็น่าจะทราบกันดีอยู่แล้วว่าเกมไหนที่น่าเล่น เพราะคงเคยเล่นมาหมดแล้ว แทบจทุกเกมก็เป็นได้ สำหรับมือใหม่ที่ยังไม่รู้ ว่าถ้าเกิดสมัครสมาชิกเข้าไปแล้ว จะเล่นเกมอะไรดีที่จะได้เงินดีๆ บางคนอาจจะเล่นไม่เป็น แต่มันก็คงไม่ใช่ปัญหาอะไรเลย ทางเรามีพนักงานคอยให้คำปรึกษา และคอยสอนท่านด้วย คุณอยากลองเล่นเกมไหน็ให้พนักงานสอนได้ และ วันนี้เราจะมา แนะนำ เกม ค่า สิ โน ออนไลน์ จัดอันดับคาสิโนที่ดีที่สุดในโลก เพื่อเป็นการช่วยตัดสินใจให้ผู้เล่น ที่จะมาเป็นสมาชิกใหม่ของเราด้วย

ReplyDeletebetflixเทคนิคการเล่นเกม PG SLOT เพื่อเพิ่มกำไร betflix วันนี้เรามาเอาใจผู้เล่น เดิมพันออนไลน์ วิธีเล่นเกมให้ชนะ สายลงทุนไม่ควรพลาด ด้วยเทคนิค การเล่นขั้นเทพ เล่นแล้วได้เงินชัวร์ 100 % เห็นผลกำไรแน่นอน เกมสล็อต เล่นได้ง่าย ได้เงินเร็ว

ReplyDeleteในทุกวันนี้ การเล่นคาสิโนออนไลน์ การใช้ สูตรสล็อต ในการเล่นสล็อตทุกค่าย MEGA GAME เพื่อใช้ในการ เล่นสล็อตก็คือ เลือกสล็อต เว็บตรง ที่มีความน่าเชื่อถือ ไม่มีประวัติการโกง การันตีเรื่องการเงิน อันดับแรกให้ นักเสี่ยงโชคผู้เล่น สังเกตจำนวน ผู้เข้าใช้บริการก่อน เพราะถ้าเว็บไหน มีจำนวนนักเสี่ยงโชค ใช้บริการมาก ถือว่าเว็บนั้น มีความน่าเชื่อถือ สำหรับเกม betflix ที่ควรเลือกเล่น เราขอแนะนำว่า คุณควรเลือกเกม ที่มียอดบิดไม่สูงมาก เพราะถ้าคุณ betflik มีทุนที่จำกัด จะได้มีโอกาส ในการทำเงินมากขึ้น ส่วนเกมสล๊อตที่อยาก แนะนำให้นักเสี่ยงโชคเล่น ก็คือเกมที่มี นักเสี่ยงโชคผู้เล่น เข้าเล่นไปเล่นจำนวนมาก เพราะนั่นหมายถึงว่า เกมนั้นจะมี อัตราออกบ่อยแน่นอน ทดลองใช้สูตรสล็อตฟรี และนี้ก็คือสูตร การเล่นสล็อต ทุนน้อย ที่ทำง่ายและใช้ได้ผลจริง สำหรับใครที่กำลังมองหา เว็บสล็อตที่โบนัส แจ็คพอตแตกบ่อย เราขอแนะนำ MEGA MAGE

ReplyDeletebetflixเกมส์ สล็อต Big Bad Wolf จากค่าย Quickspin ที่เปิดตัวมาสักพักใหญ่ๆ แต่ก็ยังมีผู้เล่น ที่สามารถสร้างกำไร จากการเล่นสล็อต มาอย่างต่อเนื่องยาวนานเป็นสล็อตออนไลน์ ที่หยิบยกเทพนิยาย สีสันและสดใส เกมที่ออกแบบมาอย่างดี

ReplyDeleteMEGA GAME MEGA GAM สูตรเล่นสล็อต ให้แจ็คพอตแตก ภายในไม่ถึง 30 นาทีไม่เสียทุนท่าน แถมกำไรแบบจุใจกลับไปกอดฟินๆอยู่บ้าน เหมาะมากสำหรับผู้ เล่นมือใหม่ไม่ลองถือ ว่าท่านพลาด อย่างหนักเรา ขอรับประกันเลย ว่ามีแต่ได้กับได้ไม่มีเสียแน่ นอนถ้าท่าน ทำตามสูตรของเรา คลิกเลย! สล็อตเล่นง่ายแตก บ่อยได้เงินจริงต้อง ที่นี้ที่เดียวกับเว็บไซต์ MEGA GAME

ReplyDeleteการที่นักเสี่ยงโชค เลือกเล่นเกมสล็อตของ เกม PGSLOT จะทำให้นักเสี่ยงโชคทุกท่านนั้น เข้าใจกับรูปแบบและกติกา ของเกมนั้นๆมากขึ้น เพราะเกม สล็อตสร้างรายได้ง่ายๆ betflix มีหลากหลายชนิดมาก และหลากหลาย รูปแบบ กฎกติกา ก็ได้มีรูปแบบ ที่แตกต่างกันออกไป ดังนั้นนักเสี่ยงโชค betflik ผู้เล่นควรจะต้องศึกษา และเรียนรู้รูปแบบ ของเกมนั้นๆให้ดีเสียก่อน หรือ ทดลองเล่นpg เพราะมันจะสามารถช่วย ทำเงินให้นักเสี่ยงโชค ทุกท่านได้ง่ายขึ้น ไม่ว่าคุณจะเล่นด้วยเงิน ที่ลงเดิมพันที่เยอะ หรือน้อยก็ตาม โดยจริงๆแล้วระบบเกม slotแตกเยอะ อัตราส่วนที่นักเสี่ยงโชคทุกท่าน จะได้เงินรางวัล จากเกมนั้นไม่ยาก จนเกินไป

ReplyDeleteMEGA GAME สล็อตแตกดี การเล่นสล็อออนไลน์ไ ด้อย่างไม่จำกัดเวลา ไม่แปลกที่ทุกท่านจะคาด หวังกับเงินรางวัล ที่ได้กลับมา ทางเว็บของเรากำลัง จะได้รับรวมทั้งเลือก หาเว็บ MEGA GAME แตกง่าย ในปัจจุบัน ที่ตามมาตรฐานกำหนดและก็พร้อมที่ จะแจกเงินรางวัล ของจริงแท้ PGSLOT ไม่ทุจริตอย่างแน่นอน ทางเว็บของเรา ได้เลือกเล่นสล็อต เว็บไซต์ที่เป็น PGSLOT

ReplyDeleteMEGA GAME พิเศษ ล็อคอินฟรี ปั่นสล็อตออนไลน์ MEGA GAME บริการ 24 ชั่วโมง ท่านไม่ต้อง เสียค่าใช้ จ่ายแม้แต่บาท เดียวท่านก็สามารถ เล่นสล็อต กับเราได้ แล้ววันนี้ ทำเงินได้จริง เบิกได้จริง เรารับรองได้เลย ไม่ได้มีที่ไหน แต่มีที่เมก้าเกม ที่นี่ที่เดียวเท่านั้น เพียงท่านสมัคร สมาชิกกับเราวันนี้ ถ้าสามารถ รับสิทธิ์พิเศษ มากมายที่ท่านไม่เคย เห็นที่ไหนมาก่อน เฉพาะสมา ชิกเท่านั้น เว็บสล็อตที่ใครๆ

ReplyDeleteBETFLIX ใครที่กำลังมองหาเว็บเดิมพัน ไว้แทงไฮโล เว็บไซต์เราได้ถูกคัดสรรมาเป็นเว็บอันดับต้นๆ BETFLIX ผู้เดิมพันต้องทำความเข้าใจก่อน ว่าเกมไฮโล คืออะไร แล้วมีกติกาการเล่นยังไง มีอัตราการจ่ายยังไง ปัจจุบันการเล่น ไฮโลไทยออนไลน์ ได้ถูกจัดมาเป็นหนึ่งในเกมพนันออนไลน์ โดยวิธีเล่นไฮโลไทย ผู้เล่นต้องเข้าใจก่อนว่าเว็บทุกเว็บๆเปิดให้เล่น mega game แต่ก็ไม่ใช่ทุกเว็บไซต์ที่จะให้ความรู้สึกมั่นคง ปลอดภัยในการเล่นเหมือนกันหมด ดังนั้นการเล่นเกมไฮโล ผู้เล่นต้องเลือกเว็บไซต์ ไฮโลออนไลน์ ดีที่สุด และปัจจุบันก็ต้องยกให้ที่ BETFLIX ไฮโลไทยออนไลน์ 100% รวมค่ายเกมไฮโลชั้นนำไว้มากมาย megagame

ReplyDeletebetflixเปิดสนามประลอง กับสัตว์ที่แข็งแกร่งที่สุดใน การประลองการต่อสู้ Tiger Glory สู่สังเวียน โคลอสเซียม กรุงโรม เกมสล็อตออนไลน์ ที่มาในธีม การต่อสู้กลาดิเอเตอร์ นักรบที่ยิ่งใหญ่ เพื่อเอาชนะ เสือดุร้ายที่แข็งแกร่ง ที่มีประวัติศาสตร์ มาอย่างยาวนาน มาร่วมต่อสู้ เพื่อค้นหา สัญลักษณ์พิเศษ และฟีเจอร์ฟรีสปิน และรางวัลโบนัสแจ็คพ็อตแตก จาก ค่ายเกมส์สล็อต เล่นเกมสร้างรายได้ เล่นเกมได้เงินจริง Tiger Glory เกมสร้างรายได้ เว็บสล็อตยอดนิยม ที่ betflix เว็บสล็อตแตกเยอะ

ReplyDeleteMEGA GAME สล็อตมือถือ คืออะไรมาดูกัน เกมฮิตบนมือถือ MEGA GAMEสำหรับการเล่นเกมสล็อตหรือออนไลน์ในมือถือนั้นเป็นอีกช่องทางใหม่ในการเข้าการเล่นเกมและเดิมพัน ซึ่งพัฒนาเพิ่มเติมจากในการเล่นบนคอมพิวเตอร์ เพื่อตอบสนองผู้เล่นในยุค 5Gนั่นเอง PGSLOT ที่มักจะใช้งานสมาร์ทโฟนหรือโทรศัพท์มือถือทำเงินกิจกรรมต่าง ๆ ดังนั้น จึงเป็นช่องทางในการเล่นสล็อตของเกมออนไลน์

ReplyDeleteBETFLIX สล็อตเกมที่มาแรงที่สุดในปัจจุบันนี้ เว็บ BETFLIX ของเรามีเกมสล็อตมากมายหลายแบบ ให้คุณสมัครเข้ามาเลือกเล่น เลือกสนุกกับ สล็อตออนไลน์ ได้ทุกที่ทุกเวลา ท่านสามารถ เล่นสล็อตผ่านมือถือ ไอแพด แท็ปแล็ต ทั้งในระบบ IOS และ Android ที่คุณพกพาไปด้วยได้ ตลอดเวลา megagame หรือคุณจะเล่นในคอมพิวเตอร์ หรือโน๊ตบุ๊คก็สามารถเล่นได้ เช่นกัน เว็บคาสิโน ของเราเป็นเว็บที่การเงินมั่นคง คุณสามารถฝาก-ถอน ได้ทุกเวลา เว็บนี้จึงเป็นเว็บที่เหมาะกับนักลงทุนเดิมพันมากที่สุด หากชื่นชอบการเล่นเกมสล็อตออนไลน์ ยินดีให้บริการกับทุก ๆ คนตลอด 24 ชม. พร้อมนำเสนอความพิเศษ ในแบบที่ใครก็ชื่นชอบ เล่นสล็อตออนไลน์ บน มือ ถือ กลายเป็นสิ่งที่กำลังได้รับความนิยม แล้วมันดีพอเหมือนกับการเล่นผ่านหน้าเว็บหรือไม่ เล่นแล้วเป็นอย่างไรบ้าง คำตอบต่าง ๆ จะถูกนำมาเฉลยกันในบทความนี้แล้ว mega game

ReplyDeletebetflix

ReplyDeleteวันนี้เรามาดู ข้อดีการเล่น เกมสล็อต จากเว็บ betflix กัน ถือได้ว่า เป็นการเล่นเกม สล็อตออนไลน์ ที่ง่ายที่ทุก ๆคน ก็สามารถเล่นได้ เพียงแค่ท่าน มีอินเตอร์เน็ตมือถือ มีเงินเพื่อเดิมในพันเกม สำหรับการเล่น จากนั้นก็สามารถ สมัครเข้ามาเล่น กับทางเว็บได้เลย จุดเด่น ของเกมสล็อต เวลาไหน ก็สมารถรอลุ้น เงินรางวัลได้เลย ไม่ยุ่งยากเสียเวลา

MEGA GAME พิเศษ ฝากถอนเร็วทันใจ ที่ MEGA GAME ท่านใช้เวลาไม่ถึง 10 วิ ท่านสามารถ เล่นสล็อต ได้ลุ้นได้ตลอดทั้งเกม ลงทุนน้อย เริ่มเดิมพัน เพียง 1 บาทเท่านั้นจ้า รับโบนัสได้เพียบ ตั้งแต่ครั้งแรก ที่เป็นสมาชิกกับ MEGA GAME และสิทธิอื่นๆ อีกมากมาย สำหรับสมาชิก ของเราโดยเฉพาะ เป็นหนึ่งในจุดเด่น ที่เรา แนะนำว่าต้องมาสัมผัสด้วยตัวเอง เดิมพันสุด

ReplyDeletebetflix

ReplyDeleteCasino เล่นง่ายบนมือถือ แหล่งรวมเกม casino online ทำเงินง่าย ได้เงินจริง ปลอดภัย สามารถเข้าเล่นได้ จากทุกแพลตฟอร์ม ตลอด 24 ชั่วโมง เหมาะกับนักเสี่ยงโชค ที่กำลังมองหาช่องทาง ในการทำเงิน ซึ่งเว็บ Betflix ของเราได้รวม Casino Online บน มือ ถือ เดิมพัน ออนไลน์ ทำเงินง่าย ไว้มากมาย รวมถึง เกมสล็อต ที่ได้รับความนิยมมาก

BETFLIX ทางเข้า เล่นเกมสล็อตออนไลน์ BETFLIX ลิงค์ตรงที่เชื่อมต่อเว็บพนันสล็อต ชื่อดังที่มีสล็อตแบรนด์ รายใหญ่ให้เล่นมากกว่า 11 บริษัทชั้นนำ และ เว็บไซต์ XOSLOTZ ของเราเป็นบริการเว็บรายใหญ่ที่พร้อมจะ ทำให้สมาชิกสมัครฟรี ไม่เสียค่าใช้จ่ายภายใต้ ระบบฝากถอนอัตโนมัติที่ทันสมัย และ มีลิงค์ทางเข้าที่ปลอดภัย เชื่อมต่อความบันเทิงต่างๆได้ทันใจ megagame ยังมีตู้เกมสล็อตออนไลน์ ขนความสนุกมาเป็นตัวเลือกให้คนมากกว่า 1,000 เกมทำให้พื้นที่แห่งนี้เป็น แหล่งรวมเกมสล็อตออนไลน์ xoslot ทางเข้า ที่ใหญ่ที่สุด และ ยังมีแบรนด์ชั้นนำให้เล่น อย่างจุใจกลายเป็นเว็บไซต์ที่พร้อมจะ ทำให้คุณสนุกกับสล็อตออนไลน์ได้มากที่สุด megagame

ReplyDeletebetflix

ReplyDeleteการเล่นเกม ยิงปลาง่าย ได้เงินจริง ไม่ได้มีเงื่อนไข หรือกติกาอะไรที่ยุ่งยาก แค่ผู้เล่นต้องรู้ เทคนิค การเล่นเกมยิงปลา เล่นยังไงให้ได้เงิน และ ทำกำไรจากการเล่น Betflix เป็นเว็บเกมยิงปลาออนไลน์ ที่เล่นเกมได้เงินจริงๆ ไม่ว่าจะเป็นเดิมพัน เกมชนิดใดๆ เกมยิงปลาฟรีเครดิตถอนได้ ต้องล้วนต้องศึกษาดู กติกาเงื่อนไข ต่างๆ ในเกมก่อน ทำการเดิมพันทั้งนั้น

MEGA GAME เพื่อนๆ สงสัยกันไหมว่า ระบบ MEGA GAME ดียังไง เราต้องบอกก่อนเลยว่า เว็บไซต์ของเรา เป็นเว็บไซต์ที่ พึ่งถูกเปิดตัวได้ไม่นานมานี้ และเป็น เว็บเกมสล็อตยอดนิยม เว็บสล็อต ที่ มี คน เล่น มาก ที่สุด 2021 แต่ด้วยความ พิเศษมากมาย จึงทำให้เป็น ที่น่าจับตามอง แล้วมีผู้เล่น ให้ความสนใจอย่างล้นหลาม กับจุดเด่นที่ ผู้ที่เคยเข้ามาเล่น ต่างก็ต้องตื่นตา ตื่นใจ ไปกับระบบ

ReplyDelete

ReplyDeleteMEGA GAME คอเกมสล็อต XO ค่ายใหญ่ทั้งหลาย ทุกท่านสามารถเข้าเล่นเกมกับทางเว็บเราได้แล้ววั้นนี้ กับเกมสล็อต XO จากทางหน้าเว็บของเรานั่นเอง โดยการเล่นนั้นไม่ผ่านเอเย่นต์ ใด ๆ MEGA GAME สล็อตXOค่ายใหญ่ ทั้งนั้น หรือผู้ เล่นทุกท่านสามารถเล่นผ่านทางโทรศัพท์โดยตรง หรือเล่นผ่านทางเว็บไซต์ หรือแอปพิเคชั่น ต่าง ๆ จากช่องทาง ที่เรากล่าวมานั้น ล้อนเป็นช่องทางที่มีคุณภาพครบครัน

BETFLIX สล็อตออนไลน์พื้นฐาน BETFLIX สำหรับมือใหม่ เป็นอีกหนึ่งเกม ที่ผู้เล่นเยอะมากกว่า 10,000 คนต่อวันได้รับ ความนิยมไปทั่วโลก ด้วยรูปแบบที่เล่นง่าย ไม่ซับซ้อน เล่นได้ผ่านเว็บไซต์หรือแอปพลิเคชันมือถือ ไม่ต้องใช้ หลักการอะไรมากมาย และ มันยังทำให้เราได้กำไรก้อนโต วิธีเล่นสล็อต สล็อตออนไลน์ megagame ก็เลยมีอิทธิพล กับแฟนตัวยงทั้งไทย และ ต่างประเทศ ให้ความสนใจมากที่สุด เทคนิคการเล่นสล็อต ให้ได้โบนัส pg ให้ได้เงินที่คนส่วนมากยังไม่รู้ หลังจากที่ผู้เดิมพันอ่าน และ เข้าใจรายละเอียด ผู้เดิมพันจะสามารถเล่นเกม สล็อต ออนไลน์ให้ชนะ และ รับรองเลยว่า หลังจากผู้เดิมพันอ่าน กำไรอย่างไม่ยากเย็น เหมือนที่ผ่านมาแน่นอน megagame

ReplyDeleteBETFLIX สำหรับ ผู้เล่นที่เป็นนักพนันยุคใหม่ BETFLIX คือ เว็บพนันยุคใหม่ จะเป็นอีกหนึ่งช่องทาง ที่สามารถตอบโจทย์คุณ ได้เป็นอย่างดีแน่นอน เพราะเราคืออีกหนึ่งเว็บ เดิมพันที่มาแรงมากในปัจจุบัน และเรายังได้ รวบรวมเกมเดิมพัน ให้คุณได้สัมผัส อีกมากมาย บอกได้เลยว่าเราจะเป็นช่องทางที่คุณ จะได้เข้ามาทำกำไร บวกกับได้เล่นเกมที่ได้คุณภาพอย่างแน่นอน

ReplyDeleteMEGA GAME ท่านรู้หรือไม่ว่าในเวลานี้การเล่นเกมคาสิโนกำลังได้รับความสนใจมากขึ้นเรื่อยๆ และในยุคแห่งความทันสมัยนี้ก็ได้มีการบริการเกมคาสิโนในรูปแบบของ คาสิโนสด ให้ได้ร่วมสนุกกันแล้ว ซึ่งจะทำให้ผู้เล่นได้รับทั้งความสนุก ตื่นเต้น และความสมจริงกับการเดิมพันแบบสด ๆ MEGA GAME ที่จะได้รับความรู้สึกเหมือนกับว่ากำลังนั่งเล่นอยู่ที่สถานที่จริง โดยจะเป็นระบบที่มีการไลฟ์สดมาจากบ่อนคาสิโนจริงทั่วโลก

ReplyDeleteสล็อตในวันนี้เราจะพาผู้เล่นทุกคนมาพบกับ เว็บสล็อตมาแรง ที่ MEGA GAME betflix จะมาเปลี่ยนความน่าเบื่อ ของท่านให้กลาย เป็นเรื่องสนุก เป็นเว็บที่รวมคุณภาพ มากกว่าใครๆ มีระบบทันสมัย เข้าเล่นไม่มีสะดุด มีผู้เล่นทั่วโลกให้ความไว้วางใจ เข้าร่วมเล่น เว็บสล็อตใหม่ล่าสุดเว็บตรง มีโปรโมชั่นเจ๋งๆ มามอบให้กับผู้เล่นได้รับกันไปเต็มๆ มีเกมสล็อตจากค่าย

ReplyDeleteBETFLIX เข้าเล่นเกมสล็อต หลายๆคนคงเคยได้ยิน มาว่าการเล่นเกมสล็อตออนไลน์ BETFLIX ในเว็บไซต์นั้น อาจจะโดนโกง หรือ ไม่ได้รับเงินจริง ๆ เลยรู้สึกว่าไม่กล้าลอง เข้ามาเล่น หรืออาจจะฟังจากคนอื่น มาว่าเล่นไปก็ไม่ได้รับเงินจริง ๆ หรอกทำให้รู้สึก ลังเลว่าจะเล่นดีไหม แต่ว่ามันจะไม่เป็นอย่างนั้น แน่นอนถ้าหากเรา เลือกเล่นเกมสล็อตออนไลน์ จากเว็บไซต์ BETFLIK11 ที่มีมาตรฐาน และ มีความน่าเชื่อถือ เพราะว่าหลายคน ที่เคยเจอประสบการณ์ ที่เล่นแล้วไม่ได้เงิน หรือ ว่าเล่นแล้วโดนโกงนั้น อาจจะมาจากการ ใช้บริการจาก เว็บไซต์ที่มีการโฆษณาที่เกินจริง

ReplyDeleteBETFLIX เกมสล็อตออนไลน์ BETFLIX เกมที่สร้างขึ้นมา ในรูปแบบที่ให้เกมเล่นง่ายที่สุด กราฟิก และ เสียง คมชัด ระดับ 4K มีเกมทุกรูปแบบ ทุกค่าย ไม่เพียงแต่สล็อตเท่านั้น ยังมีคาสิโนอื่นๆอีกมากมาย สล็อต ได้เงินจริง ในปัจจุบันนี้ก่อนที่นักเดิมพัน จะตัดสินใจเลือกเข้าไปเล่นเกมได้บนเว็บออนไลน์ ก็ควรต้องดูให้ดีว่าเกมนั้นเล่นง่าย หรือว่าจ่ายเงินจริงให้กับผู้เล่นหรือไม่ โดยการเล่นเกมสล็อต megagame สล็อต เว็บไหน ได้เงินจริง กับเว็บของเรา ก็จะทำให้ได้เล่นเกมง่ายเป็นร้อยเกมเลยทีเดียว และ ทำให้ได้รับการจ่ายเงินจริงทุกครั้งอีกด้วย ซึ่งการเล่นเกมกับเราก็จะทำให้ผู้เล่นไม่ต้องเดิมพันแบบมีรูปแบบให้ใช้ยุ่งยากอีกด้วย megagame

ReplyDeleteMEGA GAME โดยในสิ่งที่สำคัญเป็นอย่างยิ่งก่อนที่จะตัดสินใจในการเข้ามาร่วมเดิมพันผ่าน สล็อตเว็บตรง มีใบเซอร์ ใบรับรองจากสถาบันชั้นนำมากมายต่างๆ ที่จะทำให้เป็นสิ่งบ่งชี้ชัดเจนให้กับความปลอดภัย ที่ตามมาด้วย ความมั่นคงใน ทันทีในตาเห็น และในเว็บ MEGA GAME ของเรานี้ยังคง ได้รวมค่ายสล็อตออนไลน์ ไว้ครบครัน หมดแล้ว ที่พร้อมยินดีให้บริการแก่ทุกท่าน ได้ ตลอดเวลา

ReplyDeletebetflixสวัสดีนักเสี่ยงโชคทุกท่าน วันนี้จะมาแนะนำ BETFLIX สล็อตฟาโรห์ล่าสุด แน่นอนว่าเป็นอีกหนึ่งเกมดัง ที่ได้รับความนิยมสูง โดยทางเราได้รับลิขสิทธิ์แท้ สล็อต ฟาโร ได้มีการเผยแพร่ เกมชั้นนำอย่าง สล็อตแตกหนัก ที่ได้อัปเดตความสนุก ใหม่ในรูปแบบ 2022 เลือกเล่นผ่านเว็บตรง ไม่ผ่านเอเย่นต์ การันตีด้วยคุณภาพ เล่นง่ายปลอดภัย ได้เงินจริง ท่านสามารถสนุกกับเกม สล็อตย้อนยุค ที่มาพร้อมกับความสนุก ในรูปแบบใหม่ๆ

ReplyDeleteสล็อต ท่านจะได้พบกับ megagame-auto คือเกมที่เล่นผ่าน MEGA GAME ระบบออนไลน์ ให้ท่านได้เล่นเกมบนมือถือของท่านเอง ไม่ต้องผ่านแอพอะไรทั้งสิ้น เพราะสมัครกับเราได้ง่ายๆ ไม่ต้องเสียเงินท่าน แม้แต่บาทเดียว เล่นกับเราได้เงินแน่นอน เว็บของเราเว็บสล็อต ค่ายชั้นนำที่มีผู้เล่นมากที่สุด เว็บเมก้าเกมสล็อต เกมสล็อตยอดฮิต ใหม่ล่าสุด รวมค่ายเกม

ReplyDeleteThis website has emerged as my favorite as I regularly spot important subject matter on this website.

ReplyDeleteurl opener

online filmek

ฟีเจอร์การเล่นสล็อตจากค่าย MEGA SLOT แบบลองเล่นแบบฟรีๆ ไม่มีค่าบริการกับฟังก์ชั่น ทดลองเล่นสล็อต ฟีเจอร์เข้าเลือกเล่นได้มากกว่า 250 วิดิโอสล็ฮตผ่านทเว็ป https://www.megaslot.game/play-demo/

ReplyDeleteFor many people this is important, so check out my profile: antminer L7

ReplyDeleteyoure so cool! I donstw fon this net web page , i love it. Im no professional, but i remember you simply made the excellent factor. You clearly know what youre talking about, and i can truly get behind that. Thanks for being so prematurely and so honest. 먹튀사이트

ReplyDeletehowdy. Neat publish. There's an trouble along with your web site in firefox, and you may need to check this… the browser is the market chief and a large part of different humans will omit your incredible writing because of this hassle. Notable statistics in your blog, thanks for taking the time to share with us. Exceptional insight you've got on this, it's first-class to discover a internet site that information a lot records approximately special artists. Thank you high-quality article. After i saw jon’s e-mail, i realize the publish will be good and i am surprised which you wrote it guy! 안전놀이터

ReplyDeletei'm unable to examine articles online very regularly, but i’m glad i did these days. This is thoroughly written and your factors are well-expressed. Please, don’t ever stop writing. That appears to be outstanding but i'm nonetheless not too certain that i really like it. At any price will look some distance extra into it and determine in my view! Best aspire to say ones content material can be as great. This clarity with your post is first rate and that i might imagine you’re a guru for this problem. First-rate in conjunction with your concur allow me to to seize your cutting-edge give to maintain changed through the usage of approaching weblog publish. Thanks plenty hundreds of at the side of you should move on the pleasing get the activity accomplished. High-quality article, it become especially helpful! I actually began on this and i'm turning into more acquainted with it better. The post is written in very an awesome way and it contains many beneficial information for me. Thank you very a great deal and could search for more postings from you . Satisfactory to be journeying your weblog once more, it has been months for me. Nicely this newsletter that ive been waited for therefore lengthy. I want this text to finish my challenge inside the school, and it has same subject matter together with your article. Thanks, excellent share. Awesome statistics. This weblog appears just like my antique one! It’s on a completely distinctive topic 사다리사이트

ReplyDeletehmm it seems like your website online ate my first comment (it became extremely long) so i guess i'll simply sue and a amazing topic as properly i certainly get amazed to examine this. Its definitely exact. 토토핫보증업체

ReplyDeleteSuperb website and a amazing topic as properly i certainly get amazed to examine this. Its definitely exact. 토토코드거래소

ReplyDeletesure i am absolutely agreedeated imposing huge quantity beyond running experience. I'd like to see the entire works very a great deal. 안전놀이터

ReplyDeleteIt is extremely useful for me. Thank you for this sort of precious help once more. 메이저놀이터순위

ReplyDeletesplendid information! I recently got here across your weblog and had been analyzing alongside. I notion i might depart my first comment. I don’t understand what to mention besides that i have. I simply respect the form of topics you publish right here. Thanks for sharing us a exceptional information that is without a doubt beneficial. Top day! Thanks very a lot for this useful article. I love it. That is an notable motivating article. I am practically happy together with your remarkable paintings. You placed genuinely extraordinarily supportive statistics. Preserve it up. Retain running a blog. Hoping to perusing your next put up 메이저공원

ReplyDeletethanks for sharing this facts. I truely like your blog submit very a good deal. You have certainly shared a informative and interesting blog post . You beget a completely exciting internet site. I just like the full statistics that you provender with every article. Very quality article, i loved studying your put up, very satisfactory percentage, i need to twit this to my fans. Thank you! Wow, first rate, i was wondering a way to remedy acne certainly. And observed your web page via google, found out a lot, now i’m a piece clear. I’ve bookmark your web page and additionally upload rss. Keep us up to date. I used to be browsing the internet for data and got here throughout your weblog. I am inspired by using the information you have in this weblog. It shows how nicely you apprehend this challenge. Handiest aspire to mention ones content can be as notable. This readability together with your post is brilliant and that i may think you’re a guru for this problem. Extraordinary along with your concur permit me to to seize your modern-day give to hold modified via the use of drawing close weblog publish. Thanks loads hundreds of in conjunction with you need to go at the pleasurable get the job performed. 카지노추천

ReplyDeletehigh-quality to satisfy you. Your pu off danger that lone i have the possibility. Thank you for sharing this informative put up with us, preserve sharing it in the future 메이저놀이터모음

ReplyDeleteright publish but i was thinking if you may write a litte extra on this difficulty? I’d be very grateful if you could difficult a bit bit in addition. Admire it! I truely loved analyzing your weblog. It was thoroughly authored and easy to undertand. Unlike additional blogs i have examine which are simply not tht suitable. I additionally located your posts very interesting. In fact after reading, i had to cross display it to my friend and he ejoyed it as well! This put up is right sufficient to make any person recognize this fantastic element, and i'm certain absolutely everyone will respect this interesting matters . I'm able to’t agree with focusing long sufficient to investigate; plenty much less write this sort of article. You’ve outdone yourself with this material really. It's far one of the finest contents. I feel very thankful that i study this. It's miles very beneficial and very informative and that i truly found out lots from it . That is a extraordinary article, given this kind of superb quantity of data in it, those sort of articles maintains the customers enthusiasm for the web page, and hold sharing greater ... Thank you for sharing high-quality facts. It is pleasant to examine such terrific content material. Thank you for the put up 메이저공원

ReplyDeleteexceptional study, superb website, wherein did u provide you with the statistics in this posting? I have read many of the articles on your website now, and i virtually like your fashion. Thanks a million and please preserve up the effective paintings i trully appretiate your work and recommendations given with the aid of you is beneficial to me. I will proportion this facts with my family & pals. That is a outstanding internet site, hold the high quality critiques coming. That is a excellent inspiring . I am pretty an awful lot thrilled together with your correct work. You put virtually very helpful records. I'm seeking to analyzing your subsequent put up. !!!! 먹튀폴리스

ReplyDeletethanks for sharing this facts. I truely like your blog submit very a good deal. You have certainly shared a informative and interesting blog post . You beget a completely exciting internet site. I just like the full statistics that you provender with every article. Very quality article, i loved studying your put up, very satisfactory percentage, i need to twit this to my fans. Thank you! Wow, first rate, i was wondering a way to remedy acne certainly. And observed your web page via google, found out a lot, now i’m a piece clear. I’ve bookmark your web page and additionally upload rss. Keep us up to date. I used to be browsing the internet for data and got here throughout your weblog. I am inspired by using the information you have in this weblog. It shows how nicely you apprehend this challenge. Handiest aspire to mention ones content can be as notable. This readability together with your post is brilliant and that i may think you’re a guru for this problem. Extraordinary along with your concur permit me to to seize your modern-day give to hold modified via the use of drawing close weblog publish. Thanks loads hundreds of in conjunction with you need to go at the pleasurable get the job performed. 토토사이트

ReplyDeleteway cool! Some extremely legitn with us. Please hold us up to date like this. Thank you for sharing. 토토사이트

ReplyDeleteHello I am so delighted I located your blog, I really located you by mistake, while I was watching on google for something else, Anyways I am here now and could just like to say thank for a tremendous post and a all round entertaining website. Please do keep up the great work. 스포츠토토

ReplyDeleteI really loved reading your blog. It was very we nice blog. Thank you for sharing..A very awesome blog post. We are really grateful for your blog post. You will find a lot of approaches after visiting your pos 사설토토홍보

ReplyDeletewhat to say except that I have. 토토사이트추천

ReplyDeleteYour site is very good, and this post is unique and interesting and very helpful. Thank you for sharing this wonderful information. Please visit our blog site.

ReplyDelete토토

스포츠토토

카지노

바카라사이트윈

كلادينج هو عبارة عن ألواح تستخدم لكساء واجهات المباني وتميز بخفه وزنها وعزلها للحراة ومقاومتها للحريق بالإضافة إلي مميزات كثيرة مثل تعدد الالوان وطريقة تركيبها السهلة والسريعة عن طريق التعشيق وتظهر فواصل بين الألواح وذلك يزيد من متانتها وهو الكلادينج لطريقة سهلة وسريعة

ReplyDeleteتختلف اسعار الواح الكلادينج للمطابخ تعتبر التكلفة واحدة من أبرز عيوب المطابخ الكلادينج، ولكن عندما ننظر الى عمر المطابخ الكلادينج الطويل، تصبح التكلفة معقولة، وفي حالة تلف أحد الطبقات الكلادينج يصبح من الصعب تغييرها، لان بعد تعشيق طبقات الكلادينج يصبح من السهل رؤية الفواصل بين الطبقات.

I will be waiting anxiously for this type of most suitable details as I delighted in a great deal while looking over your article.

ReplyDeleteuwatchfree

Playtubes

ในเกมสล็อตแตกง่าย ที่ไม่ซ้ำกัน ด้วยรางวัลมากมาย ได้ด้วยเกมสล็อต BETFLIX เกมสล็อตออนไลน์ที่แจ็คพอตแตกง่ายที่สุด

ReplyDeleteenjoy every game mega game789

ReplyDeleteLots of thanks for taking a part of this functional info with impressive pick of phrases.

ReplyDeleteMuhammad Ali

Akhtar Iqbal

Muhammad Usman

I appreciate to review your blog posts due to your important strategies exchanged in the blog post that not solely entertain however likewise assist us know lots of aspects.

ReplyDeleteAkhtar Iqbal

Muhammad Ali

Muhammad Usman

Lots of gratitudes for partaking this helpful points with noteworthy selection of phrases.

ReplyDeleteTheInformationCenter

Hibbah Sheikh

All News

I value your work to script this type of excellent short article. I will give out this write-up with my friends as it incorporates useful suggestions for all.

ReplyDeletehttps://bestairwaysuk.blogspot.com/

This article suffices to make an individual recognize this fantastic thing. I make sure every person will like this well-known article.

ReplyDeletehttps://bestairlinesuk1.blogspot.com/

Really enjoyable and strongly enlightening post distributed. I value your efforts to write this kind of great short article.

ReplyDeletehttps://bestdestinationsuk.blogspot.com/

I will exchange this write-up with my close friends as it includes useful information and facts for all.

ReplyDeletehttps://easyflightsuk.blogspot.com/

ReplyDeleteWith its thought-provoking exploration, compelling storytelling, and authoritative research, this blog rises above in its field.

World Travel

Best UK Travel

Fly Travel

Easy Flights

Best Destination

TRAVEL UK

UMRAH PACKAGES

ReplyDeleteUrmăriți Pe All Serialele Turcesti 2023 Netflix Online. Urmărește Serialul Românesc Gratis Online Streaming Video HD. You Can Enjoy It TV Shows And Seriale Turcesti Comedii Romantic And Filme De Dragoste Streaming For Free

Urmariti Online Serial Drama, Actiune, Drama, Si Comedie, Seriale Turcesti Vechi sau Nou in situatii foarte odihnitoare. Asta înseamnă că inima ta se simte confortabil seriale turcești comedie romantică, atât de mult încât te simți confortabil. Vă puteți bucura și, de asemenea, să împărtășiți cu prietenii și cu Faimly.

ReplyDeleteI will certainly discuss this article with my colleagues as it contains valuable information for all. I want to examine this type of building material again.

ReplyDeleteRomanian dramas in HD format

ReplyDeletehttps://klicksud.online/

Hello Everyone

ReplyDeleteHope you all doing well

Here we come again with Freshest Fullz

USA UK CANADA All states available

Full info with validity & guarantee

All fullz will be fresh not sold before

USA= NAME SSN DOB DL ADDRESS EMPLOYEE & ACCOUNT INFO FULLZ

UK= NAME NIN DOB DL ADDRESS SORT CODE & ACCOUNT NUMBER

CANADA= NAME SIN DOB ADDRESS MMN PHONE EMAIL

DL Scans & DL photos front back with selfie

High Credit Scores pros 700+ scores

Business EIN company fullz

B2B B2C Email USA UK CANADA

Contact us Here & don't forget to visit our TG channel

>TG - @ killhacks Or @ leadsupplier

>What's App - (+1) 727.. 788.. 612..9

>TG Channel - t.me/ leadsproviderworldwide

>VK Messenger ID - @ leadsupplier

>E-mail - gilberthong04 at gmail dot com

CC with CVV FULLZ with billing address

Passport Scans front back with selfie

Sweep Stakes & Loan Leads

Dumps with Pin Track 101 & 202

W-2 Forms with DL

Bank Statements & Utility Bills

Children Fullz 2011-2023

Old & young Age fullz (1955-2009)

Dead Fullz

KYC Stuff

SSN & EIN Look-up

Bulk Quantity SSN Fullz

EMAIL Leads (Crypto|Casino|Business|Company|Payday|Mortgage)

SMTP|RDP|C-PANELS

Web-Mailers|Alexus Mailer

Bulk SMS|Email Senders

Loan Methods|Carding Methods

Tools & Tutorials

Cash Out Tutorials